Profits of War: Top Beneficiaries of Pentagon Spending, 2020 – 2024

Summary

Despite the United States withdrawal from Afghanistan in 2021 and the scaling back of the “War on Terror,” Pentagon spending and contractor revenues have continued at extremely high levels, due in large part to the military’s focus on China as the new national security challenge. The U.S. arms industry has also profited enormously from the surge in foreign arms sales tied to the wars in Ukraine and Gaza.

From 2020 to 2024, the last five-year period for which full statistics are available, private firms have received $2.4 trillion in contracts from the Pentagon, approximately 54% of the department’s discretionary spending of $4.4 trillion over that period.1During those five years, $771 billion in Pentagon contracts went to just five firms: Lockheed Martin ($313 billion), RTX (formerly Raytheon, $145 billion), Boeing ($115 billion), General Dynamics ($116 billion), and Northrop Grumman ($81 billion).2By comparison, the total diplomacy, development, and humanitarian aid budget, excluding military aid, was $356 billion. In other words, the U.S. government invested over twice as much money in five weapons companies as in diplomacy and international assistance.3

Record arms transfers have further boosted the bottom lines of weapons firms. These companies have benefited from tens of billions of dollars in military aid to Israel and Ukraine, paid for by U.S. taxpayers. U.S. military aid to Israel was over $18 billion in just the first year following October 2023; military aid to Ukraine totals $65 billion since the Russian invasion in 2022 through 2025.4Additionally, a surge in foreign-funded arms sales to European allies, paid for by the recipient nations − over $170 billion in 2023 and 2024 alone − have provided additional revenue to arms contractors over and above the funds they receive directly from the Pentagon.

This year’s military budget will continue to deliver a windfall to military contractors. Recently-enacted legislation pushes annual U.S. military spending beyond the $1 trillion mark.

The trends of the past five years follow a major increase in Pentagon spending over time. Annual U.S. military spending has grown significantly this century. The Pentagon’s discretionary budget — the annual funding approved by Congress and the large majority of its overall budget — rose from $507 billion in 2000 to $843 billion5in 2025 (in constant 2025 dollars6), a 66% increase.7Including military spending outside the Pentagon — primarily nuclear weapons programs at the Department of Energy, counterterrorism operations at the Federal Bureau of Investigation (FBI), and other military activities officially classified under “Budget Function 050”8— total military spending grew from $531 billion in 2000 to $899 billion in 2025,9a 69% increase. Legislation passed in early July 202510adds $156 billion to this year’s total,11pushing the 2025 military budget to $1.06 trillion. After taking into account this supplemental funding, the U.S. military budget has nearly doubled this century, increasing 99% since 2000.

The shape of what President Eisenhower called the “military-industrial complex” is shifting as military technology companies are being awarded an increasing share of the Pentagon budget and gaining political power. The military-industrial complex involves the collaboration of the uniformed military and the arms industry in promoting spending that serves their bureaucratic interests and corporate bottom lines, often independently of or in contradiction to considerations of America’s actual security needs. Today, the tools of influence used by the arms industry are consistent — lobbying, millions in campaign donations, the revolving door, and others — but they are also expanding. One of the latest trends, for instance, is that Pentagon officials are now going on to work for venture capital firms investing in new military tech.

What remains the most important issue is whether U.S. national defense strategy is aligned with the actual security environment the U.S. faces. The current cover-the-globe strategy, which stresses a quest for military dominance and the ability to intervene anywhere on the globe in short order — has not served the U.S. well in this century. The question is whether the U.S. can have a reasoned national debate on a new defense strategy that is not distorted by the influence of the wealthy weapons sector.

Introduction

This report examines the weapons contractors which have profited from military spending between 2020 to 2024, a period that included the 2021 U.S. withdrawal from Afghanistan. During that time, which is the last five-year period for which full statistics are available, private firms have received $2.4 trillion in contracts from the Pentagon, approximately 54% of the department’s spending of $4.4 trillion over that period. The report discusses how high levels of Pentagon spending have attracted new entrants to the arms industry – emerging military tech firms. It also describes how the arms industry continues to turn profit into political power, and political power into profit.

A 2021 Costs of War report by William D. Hartung, one of the current report’s authors, described how the political climate created by the “Global War on Terror” (GWOT), launched in the early 2000s, set the stage for large increases in the Pentagon budget, much of which went to military contractors. That report spotlighted a question that has received even less attention than the costs of war: who profits from war.12The current report continues and updates this inquiry. It shows how revenues of the top U.S. arms contractors have remained at high levels due to the U.S. government’s shift from an emphasis on the “Global War on Terror” to a focus on China as the Pentagon’s “pacing threat,” accompanied by record levels of foreign arms transfers. The U.S. withdrawal from Afghanistan in September 2021 did not result in a peace dividend. Instead, President Biden requested, and Congress authorized, even higher annual budgets for the Pentagon, and President Trump is continuing that same trajectory of escalating military budgets.

Over two decades of post-9/11 wars in Afghanistan, Iraq, and elsewhere, a full $2 trillion went to just the top five contractors: Lockheed Martin, RTX (formerly Raytheon), Boeing, General Dynamics, and Northrop Grumman.13Today, a massive transfer of taxpayer dollars continues to benefit major weapons makers like Lockheed Martin and RTX. There has also been an upsurge in new contracts with tech firms that specialize in military applications of AI, swarms of drones, uncrewed ships and armored vehicles, and other emerging technologies.

The rise of these new military technology firms marks the biggest shift in the arms industry over the past five years. Companies like SpaceX, Palantir, and Anduril have been tapped for multi-billion-dollar contract awards from the Pentagon for communications, targeting, unpiloted vehicles, anti-drone defenses, and hypersonic weapons. The funds from these awards will flow to the companies over time, which should put them in the top ranks of Pentagon contractors by value of awards within the next several years. It remains to be seen whether the traditional contractors will lose business as the Pentagon shifts towards weapons using unpiloted vehicles and systems using emerging technologies like AI, or whether Pentagon budgets will rise to meet the financial aspirations of both traditional and emerging companies simultaneously.

The emerging military tech sector is the newest addition to the military-industrial complex. Emerging tech companies have outsized influence in the Trump administration, as evidenced by the role Elon Musk took as de facto head of the Department of Government Efficiency, vice president J.D. Vance’s close ties to Palantir founder Peter Thiel, and the role of Silicon Valley tech companies and the venture capital firms that invest in them in vetting candidates for the Pentagon and other key agencies and filling posts within the administration. The military tech sector is deeply embedded in the Trump administration, which should give it an upper hand in the budget battles to come.

The penetration of the administration by military tech firms, however, is part of a long-standing historical pattern of weapons contractors wielding outsized political power to continue to secure high levels of funding for the military. The ongoing influence of the arms industry over Congress operates through tens of millions in campaign contributions and the employment of 950 lobbyists, as of 2024. Military contractors also shape military policy and lobby to increase military spending by funding think tanks and serving on government commissions. These strategies are discussed in further depth in a later section.

Trends in Pentagon spending and the percentage obligated to contracts

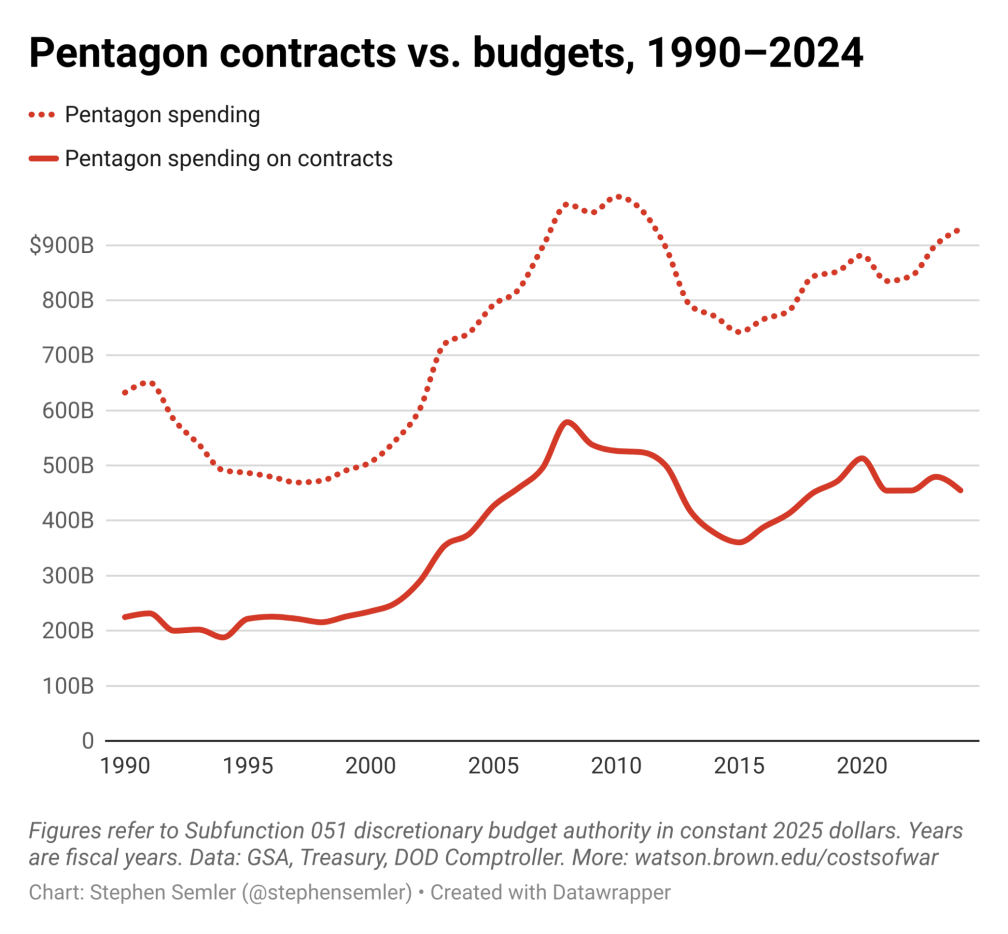

The value of military contracts obligated in a given year is determined primarily by the amount of Pentagon spending.14As Figure I shows, the value of the Pentagon’s annual contract awards generally rise and fall in step with its overall budget.15

Figure I. Pentagon Spending on Contracts vs. Overall Spending, 1990–2024 (in Constant U.S. Dollars)

Over the past 35 years, the Pentagon has devoted an increasing share of its budget to private sector contracts. For fiscal years 1990–1999, the Pentagon’s average annual spending on contracts equaled 41% of its overall spending. This has increased over each passing decade. By decade, the average percent of the Pentagon budget obligated to contracts were as follows:

- 1990–1999: 41%

- 2000–2009: 52%

- 2010–2019: 53%

- 2020–2024: 54%

From 2020–2024, the latest five-year period for which data is available, the average was 54%— $2.4 trillion in contracts, $4.4 trillion in spending. See Appendix B of this report for a full discussion of the methodology, data, and limitations behind these calculations.

Approximately $993 billion of the $1.06 trillion in military spending authorized for 2025 is for the Pentagon16(as noted above, the $1.06 trillion total also includes spending on nuclear weapons programs and other expenses outside the Pentagon). If the share of the department’s spending on contracts this year reflects the decade’s average (54%), these figures suggest a more than half-trillion-dollar transfer of wealth from U.S. taxpayers to private contractors.17

Top contractors and new military tech

From 2020–2024, the top five Pentagon contractors received $771 billion in contract awards, in constant 2025 dollars. By comparison, that amount is over twice the $356 billion that Congress appropriated for U.S. diplomacy, development, and humanitarian aid budget, excluding military aid.18

The $771 billion obligated to the top five contractors represent one-third of the total $2.4 trillion in Pentagon contract awards from 2020–2024. Lockheed Martin led the field by far with $313 billion in contract awards from 2020–2024, $168 billion more than its closest competitor, Raytheon (now RTX), which received $145 billion in contracts.

Figure II. Pentagon Contracts to Top Five Companies, 2020–2024 (in Constant U.S. Dollars)19

Lockheed Martin produces weapons systems such as combat aircraft and missiles; RTX, engines, drones and bombs; Northrop Grumman, bombers and ammunition; Boeing, helicopters and transport planes; and General Dynamics, destroyers and tanks. For a breakdown of the Pentagon’s top weapons programs — from the F-35 Joint Strike Fighter to submarines to ballistic missiles — and the companies with primary responsibility for producing them, see Appendix A.

Emerging tech firms like SpaceX, Palantir, and Anduril have received commitments of tens of billions of dollars as a result of new multi-year contracts for weapons, communications and targeting systems, but the initial awards flowing from these commitments are still in process, so these firms were not in the top ranks of Pentagon contractors as of 2024. That may change in the next several years. In addition to the emerging tech firms, big tech companies like Microsoft are now receiving major contracts from the Pentagon.20

More specifically, several of these in-process contracts for Silicon Valley firms include the following: Anduril has received awards for countering Unmanned Aerial Vehicles (UAVs) from the Marines ($642 million); a contract for its Roadrunner UAV interceptor system ($250 million); and contracts for its Ghost Shark autonomous underwater vehicle as part of the U.S.-UK-Australia AUKUS project, to name a few.21The most lucrative contract of all may be Anduril’s has also been selected to build the next generation of Army goggles, the Integrated Visual Augmentation System (IVAS), which are “intended to give soldiers everything from night-vision capability to warnings of incoming airborne threats.”22Anduril is also competing to make “collaborative combat aircraft” – unpiloted systems designed to operate in conjunction with the F-35 and F-47.23

Palantir has a $618 million contract with the Army for a data platform that utilizes artificial intelligence; a $480 million contract to continue work on the Project Maven targeting system; and a $463 million, five-year contract with the U.S. Special Operations Command to help integrate advanced commercial software into its operations.24

SpaceX receives funding to launch the majority of America’s military satellites, and is receiving funding for military versions of its Starlink system, best known for providing internet service to Ukrainian forces in their effort to fend off Russia’s attack on their country. The Pentagon is also eyeing SpaceX’s Starship system, in what the Pentagon sees as a potential means of outpacing China in the military space race. Based on the prospects for billions in new revenue from Starship and other technological developments, SpaceX’s revenues from the Pentagon are poised to grow dramatically in the next few years.25

Big tech firms are also receiving substantial Pentagon funding. To cite just one example, Amazon, Microsoft, Google, Oracle and IBM are splitting $10 billion for the Pentagon’s cloud computing program.26

To the extent that the Pentagon moves towards AI-driven weapons systems, including swarms of drones and uncrewed aircraft, ships, and combat vehicles, the dominance of the Big Five firms may be reduced. “Rebooting the Arsenal of Democracy,” an essay published on the blog of the emerging tech firm Anduril, dismisses the current big contractors as remnants of the Cold War that need to be supplanted if America is to take the lead in developing and producing the weapons of the future:

“Why can’t the existing defense companies simply do better? The largest defense contractors are staffed with patriots who nevertheless do not have the software expertise or business model to build the technology we need. Tomorrow’s weapons – autonomous systems, cyberweapons and defenses, networked systems, and more – are enabled through software, while these companies specialize in hardware. These companies work slowly, while the best engineers relish working at speed . . . These companies built the tools that kept us safe in the past, but they are not the future of our defense.”27

Not all of the funds spent on major weapons systems are spent well, to put it mildly. Tens of billions of dollars are allocated for weapons systems such as the F-35, the Sentinel intercontinental ballistic missile, (ICBM), the Littoral Combat ship, and aircraft carriers that have experienced major cost overruns, had serious performance issues, or are of questionable value for the most likely conflicts of the future.28Elon Musk, the driving force behind the Trump administration’s Department of Government Efficiency, has called the F-35 “the worst value for money” of any U.S. combat system, and has suggested that it should be cut back in favor of increased investments in unpiloted systems.29

But as Roberto González has noted in a paper for Costs of War, there is no guarantee that emerging tech firms will do any better: “[T]he priorities of the tech industry, the peculiarities of venture capital (VC) funding structures, and Silicon Valley’s startup model are likely to lead to costly, high-tech products that are ineffective, unpredictable, and unsafe when deployed in real world conditions.”30

Given the mixed performance of the arms sector — with major cost overruns and performance problems exhibited by major systems like the F-35, the Sentinel intercontinental ballistic missile (ICBM), the Littoral Combat Ship, and others — the question arises whether additional funding for the Pentagon will produce additional defense capability.

Cashing in on conflict: Global arms sales

Foreign arms transfers, including sales paid for by other nations as well as military aid paid for by U.S. taxpayers, provide an additional source of revenue for weapons contractors above and beyond what the Pentagon spends on purchasing equipment and services for the U.S. military.

The U.S. announced a record volume of major arms deals in 2024, the final year of the Biden administration — $145 billion in all, including tens of billions to Ukraine and Israel, and a huge surge in sales to Europe.31The figure is essentially indistinguishable, adjusted for inflation, from the other highest sales year since World War II, which occurred in 2011 under the Obama administration. The Obama sales surge was based on major deals to Saudi Arabia worth over $60 billion, for weapons that ended up being used in that nation’s devastating war on Yemen, which commenced in 2014 and went on for over six years.

The wars in Ukraine and Gaza have been major drivers of recent U.S. arms transfers. The U.S. has supplied over $66 billion in military aid to Ukraine since the beginning of Russia’s invasion of that country in 2022, most of it for weapons built by U.S. companies.32And Washington supplied $18.2 billion in military aid to Israel in just one year, from the start of its current military operations in Gaza in October of 2023 through September of 2024, plus at least $30 billion in commitments to future weapons sales. Offers of U.S. weapons to European allies spurred in significant part by fear of Russia topped $170 billion in 2023 and 2024 alone.33The revenues from sales to European allies, who pay for the arms, are over and above what U.S. companies receive from the Pentagon.

While President Biden touted the arms industry and its workers as the “arsenal of democracy,” a significant share of U.S. arms transfers go to undemocratic regimes or nations at war.34Since 2019, U.S. arms were possessed by one or more parties to 28 conflicts, and 31 U.S. arms clients were deemed “not free” by Freedom House.35In 2022, the Biden administration approved arms sales to 57% of the world’s autocracies, based on data from the State Department’s Directorate of Defense Trade Controls, the Pentagon’s Defense Security Cooperation Agency, and the Varieties of Democracy project.36

The breadth of U.S. arms transfers — to 107 countries from 2020–2024 — increases the risk of getting embroiled in conflicts on the side of U.S. arms recipients, whether through boots on the ground, special forces deployments, or arms transfers that help sustain or expand ongoing wars.37

Capturing Congress and the Executive Branch: Tools of influence

The arms industry has used an array of tools of influence to create an atmosphere where a Pentagon budget that is $1 trillion per year is deemed “not enough” by some members of Congress: millions in campaign and lobbying expenditures, the revolving door between the Pentagon and the weapons sector, the funding of think tanks, and the placement of current or former personnel on government commissions that shape policies pertinent to company bottom lines.38Arms industry lobbyists not only push for more funding for specific weapons systems, they also push for higher Pentagon spending overall.

Figure III: Arms Industry Tools of Influence

The vast bulk of the arms industry’s campaign contributions go to candidates for Congress. The industry favors incumbents, and concentrates much of its giving to members of the armed services committees and defense appropriations subcommittees in the House and Senate – the members with the strongest role in shaping the Pentagon budget. As of 2024, there are 950 lobbyists hired by the arms industry, 220 more than in 2020,39presumably to help the industry navigate the shift from spending on the war on terror to the new emphasis on “great power competition” and the rise of emerging military technology that may displace the traditional systems that comprise the bulk of the revenues of traditional contractors like Lockheed Martin and RTX.

Senior officials in government often go easy on major weapons companies so as not to ruin their chances of getting lucrative positions with them upon leaving government service.

For its part, the emerging military tech sector has opened a new version of the revolving door – the movement of ex-military officers and senior Pentagon officials, not to arms companies per se, but to the venture capital firms that invest in Silicon Valley arms industry startups. An investigation by Eric Lipton of The New York Times found that at least 50 former Pentagon officials went to work for military-related venture capital or private equity firms in the five years from 2019 to 2023:

“[F]ormer Pentagon officials and military officers who have joined venture capital firms . . . are trying to use their connections in Washington to cash in on the potential to sell a new generation of weapons. They represent a new path through the revolving door that has always connected the Defense Department and the military contracting business.”40

Ellen Lord, a former head of acquisitions at the Pentagon, pointed out that going the venture capital route can be considerably more lucrative than going to work for a traditional arms firm: “There’s panache now with the ties between the defense community and private equity. But they are also hoping they can cash in big-time and make a ton of money, too.”41

Contractor funding of think tanks represents another channel of potential influence. In some cases, think tanks with arms industry funding advocate for policy positions that are favorable to these companies’ bottom lines. Whether the companies fund those think tanks because they already hold such views, or whether the industry funding skews the findings of the think tanks they bankroll is not always clear, but there are clear benefits to firms like Northrop Grumman and Lockheed Martin in funding the think tank sector.

According to a 2025 Quincy Institute for Responsible Statecraft study, the top 100 military contractors contributed more than $34.7 million to the top 50 think tanks in America between 2019 and 2023. Top donors included Northrop Grumman ($5.6 million) and Lockheed Martin ($2.6 million). Top recipients of contractor funding were the Atlantic Council ($10.2 million), the Center for a New American Security ($6.6 million), and the Center for Strategic and International Studies ($4.1 million).42

A more subtle but no less important form of influence comes when individuals with ties to the arms industry serve on government advisory panels. For example, the majority of members of the Congressional Strategic Posture Commission, which wrote an October 2023 report that presented scenarios for a major buildup of U.S. nuclear forces beyond the Pentagon’s 30-year, $2 trillion plan to build new nuclear weapons, had ties to the arms industry.43The commission’s co-chair, former senator Jon Kyl, served as a lobbyist for Northrop Grumman, the lead company on the new ICBM and the new nuclear bomber, before joining the commission.

Similarly, a congressionally mandated commission charged with reviewing the Pentagon’s strategy suggested a three to five percent real increase in the department’s budget for an indefinite period. This commission also comprised a majority of members with ties to the arms sector. Its recommendations have been adopted by military hardliners in Congress, and increases in Pentagon spending in recent years have tracked its recommendations.44

Political advantage of new military tech firms in the current administration

As military tech firms like Palantir, Anduril and Space-X become an integral part of the future military-industrial complex, the question arises as to whether the weapons they propose to build will work as advertised and can be produced more cheaply and efficiently than current generation systems. If the military tech firms fulfill their promises, there could be benefits for national defense, potentially at a lower cost. But there are questions about whether these goals can be met and what strategy they will be deployed in support of, as well as serious issues related to risks posed by autonomous weapons that are deployed with little or no human input.

There may be a battle of the budget between emerging tech firms and the Big Five that will determine how much the Pentagon actually invests in emerging tech. Or, as an alternative, the Pentagon budget will soar even higher in an attempt to satisfy both the traditional contractors and the emerging military tech firms. The Trump administration will have a major role in determining which of these outcomes comes to be.

The two largest recent program announcements — Boeing’s selection as the prime contractor on the F-47 next generation combat aircraft and President Trump’s commitment to a “Golden Dome” system designed to protect the entire U.S. from incoming missiles — will offer ample opportunities to both traditional arms firms and emerging military tech companies alike. The procurement phase of the F-47 program could cost up to $20 billion, but as Dan Grazier of the Stimson Center has noted, the $20 billion is “just seed money. The total costs coming down the road will be hundreds of billions of dollars.”45At this point Golden Dome is more of an idea than a fleshed out concept, but President Trump’s goal of building a comprehensive, leakproof defense would require building large numbers of interceptors and new military satellites woven together with advanced communications and targeting systems, at a potential cost of hundreds of billions of dollars over time. This is despite the fact that, as Laura Grego of the Union of Concerned Scientists has noted, “It has been long understood that defending against a sophisticated nuclear arsenal is technically and economically unfeasible.”46That reality won’t necessarily stem the flow of massive quantities of tax dollars into the Golden Dome project, no matter how unrealistic it may be.

Given the composition of the Trump administration, the tech sector will have a political advantage in the fight for Pentagon funding, grounded in its close connections to the administration. From Elon Musk to J.D. Vance and beyond, the military tech sector has quickly developed unprecedented influence over federal regulations and expenditures. Vance worked for a venture capital firm owned by Palantir founder Peter Thiel, and his relationship with Thiel will give the military tech sector an open door to the White House.

Elon Musk’s role as de facto head of the Department of Government Efficiency (DOGE), which has played a direct role in slashing employment and funding at major federal agencies, gives the military tech sector unprecedented influence that goes well beyond the traditional clout that flows from hiring former government employees as lobbyists. Musk and the colleagues he has brought into the DOGE are literally embedded in the administration, rather than trying to influence it from the outside. And even as this occurs, Musk’s companies could benefit from any recommendations the DOGE makes about shifting funds within the Pentagon budget.

Musk and Vance are not the only advocates for the military tech sector embedded in the Trump administration.47Stephen Feinberg, second-in-charge at the Pentagon, worked for Cerberus Capital, an investment firm which has a history of investing in the gun and military industries. And Michael Obadal, a senior director at Anduril, has been selected to serve as the deputy secretary of the Army.48And a recent analysis by Bloomberg found that “more than a dozen people with ties to [Palantir founder Peter] Thiel — including current and former employees of his companies, as well as people who have helped manage his fortune or benefitted from his investments and charitable giving — have been folded into the Trump administration.”49

Conclusion

Technology alone will not save us. There is a history of failure of “miracle weapons,” either because they did not work as advertised or because they were applied to conflicts in which their capabilities were not relevant to the circumstances faced by U.S. forces. Going forward, policy makers need to be careful not to downplay the potential risks of new technologies — risks that new systems won’t work as advertised; will malfunction, causing unintended slaughter; and might make conflict more likely as the U.S. and other nations with tech-based militaries are able to put fewer troops at risk in next generation wars.50

The risks posed by AI-driven weapons are exacerbated by the hawkish tendencies and unrealistic goals of military tech leaders, who not only want a bigger share of the Pentagon pie but also want to shape how the Pentagon does business and how the U.S. conducts its foreign policy.51

The challenge is how to integrate new technology into a realistic strategy rather than simply assuming that it will be the royal route to restoring unparalleled U.S. military dominance. Part of that challenge will involve rolling back the undue influence exerted by the Silicon Valley military tech firms, who seek to dramatically increase their share of the Pentagon budget pie in the years to come, building on their close connections to the Trump administration to speed up the process. These firms should play restricted roles, not be major players in determining budget priorities and military strategy, as some of them aspire to be or already are.

The U.S. needs stronger congressional and public scrutiny of both current and emerging weapons contractors to avoid wasteful spending and reckless decision making on issues of war and peace. Profits should not drive policy. In particular, the role of Silicon Valley startups and the venture capital firms that support them needs to be better understood and debated as the U.S. crafts a new foreign policy strategy that avoids unnecessary wars and prioritizes cooperation over confrontation.

Appendix A: Contractors for the Pentagon’s largest weapons programs

A handful of firms are responsible for building the major weapons systems purchased by the Pentagon each year, as indicated by the lists of major programs carried out by the big five contractors, below. The lists are partial, focusing on the largest programs carried out by each firm.52

Lockheed Martin: combat aircraft (F-35), airlift (C-130J), helicopters (Black Hawk, CH-53K), submarine-launched ballistic missiles (Trident), tactical missiles (Hellfire, Javelin), cruise missiles (JASSM), Paveway bombs, missile defense systems.

RTX: F-35 engine, air-to-air missiles (AMRAAM, AIM-9X), air-to-surface munitions (Paveway), surveillance drones (Global Hawk), missile defense (Patriot, SM-6 missile, ballistic missile kill vehicle), tactical missiles (Sidewinder), precision guided bombs, nuclear-armed missile (Long-Range Standoff missile).

Northrop Grumman: new ICBM (Sentinel), strategic bombers (B-21), unmanned systems (Manta underwater vehicle, Fire Scout helicopter), radar planes (E-2C Hawkeye), missile defense (tracking systems), ammunition (all calibers).

Boeing: helicopters (Chinook), maritime patrol aircraft (P-8 Poseidon), transport planes (C-17), combat aircraft (F-15, F-15X, F-18), helicopter/rotary wing (Osprey, A-6 attack helicopter), Joint Direct Attack Munitions (JDAM).

General Dynamics: ballistic missile submarines (Columbia class), destroyers, tanks (M-1A2), bombs, guided munitions.

The Pentagon’s top ten weapons programs by dollar value, and the prime contractors responsible for building them, are below, based on the Pentagon’s Fiscal Year 2025 budget request.

1. F-35 Joint Strike Fighter: $12.43 billion

Prime contractors: Lockheed Martin (Airframe), Pratt & Whitney (Engine)

2. SSBN 826 Columbia Class Ballistic Missile Submarine: $9.87 billion

Prime Contractors: General Dynamics, HII

3. SSN 774 Virginia Class Submarine: $8.20 billion

Prime Contractors: General Dynamics, HII

4. DDG 51 Arleigh Burke Class Destroyer: $7.07 billion

Prime Contractors: General Dynamics Corporation, HII

5. B-21 Raider: $5.33 billion

Prime Contractor(s): Northrop Grumman

6. LGM-35A Sentinel: $3.73 billion

Prime Contractor(s): Northrop Grumman

7. KC-46A Pegasus: $2.97 billion

Prime Contractor(s): Boeing

8. CH-53K Heavy Lift Replacement Helicopter: $2.68 billion

Prime Contractors: Sikorsky Aircraft Corporation (Airframe), General Electric Company (Engine)

9. GMD: $2.52 billion

Prime Contractor(s) for current GMD: Boeing

Prime Contractors for the Next Generation Interceptor: Northrop Grumman, Lockheed Martin

10. Trident II Ballistic Missile Modifications: $2.46 billion

Prime Contractor(s): Lockheed Martin

SOURCE: U.S. Department of Defense. (March, 2024). Program Acquisition Cost by Weapon System, Fiscal Year 2025 Budget Request. https://comptroller.defense.gov/Portals/45/Documents/defbudget/FY2025/FY2025_Weapons.pdf

Appendix B: Methodology

Estimating the share of Pentagon spending that goes to contracts is mostly straightforward: divide the amount the Pentagon spends on contracts by how much it spends overall.53Contract data for this report were sourced from USAspending.gov, a federal database maintained by the Treasury Department.54 Overall spending data were drawn from the Pentagon Comptroller and the Office of Management and Budget.55Specifically, the calculation determining the share of Pentagon spending from fiscal years 2020–2024 that was obligated to contracts was as follows:

Two factors complicate this calculation — foreign arms sales and government secrecy — but they appear to cancel each other out. Foreign military sales fund Pentagon contracts, but the foreign funding involved is not counted as Pentagon spending. That raises the numerator (contract spending) without affecting the denominator (overall spending). Meanwhile, secret programs are mostly funded by the Pentagon, but their contract awards are not reported to USAspending. Because classified contract awards are not included in USAspending data, the numerator is understated, even as the associated funding remains part of the denominator.

These two factors are discussed separately below, including their respective potential effects on the estimated share of Pentagon spending obligated to contracts. Then, both factors are considered together, showing that their combined effects net a zero-percentage point change to the original estimate.

Government secrecy

Not all military contracts get reported. The U.S. intelligence budget is over $100 billion; most of it is embedded in the Pentagon budget, and it’s all classified. Per federal regulations, classified contracts are exempt from being reported to USAspending. This means that potentially tens of billions of dollars’ worth of military contracts go unreported every year.

USAspending displays the data government agencies report to it per the Digital Accountability and Transparency Act (DATA Act) of 2014. If the data is not reported, USAspending does not have access to it and cannot display it. Government secrecy is the main reason that not all contracts funded by the Pentagon are reported.

Contract obligations reported to USAspending are processed through the Federal Procurement Data System-Next Generation (FPDS-NG), which serves as the governmentwide database for procurement reporting. The Federal Acquisition Regulation (FAR) 4.606 governs these reporting requirements, outlining which contract actions agencies must report to FPDS-NG. It also lists exemptions. Because USAspending sources its procurement data directly from FPDS-NG, any contract actions exempted under this provision do not appear in USAspending’s data.56

These exemptions open up the possibility of tens of billions of dollars in military contract obligations going unreported each year. Two notable exemptions are for contracts that, if disclosed, “would compromise national security,”57and those that “constitute classified information.”58About 11% of the Pentagon budget is allocated to classified programs,59and contracts awarded through classified programs are not reported to FPDS-NG, pursuant to the exemption for classified information under FAR 4.606(c)(6).60

The Pentagon’s classified funding largely goes to the U.S. intelligence community. Most intelligence funding comes from the Pentagon budget,61and is later transferred to the intelligence agencies.62In 2024, the U.S. intelligence budget was $106.3 billion, split between the agencies under the National Intelligence Program and the Military Intelligence Program. The Pentagon manages Military Intelligence Program activities,63as well as certain activities in the National Intelligence Program, including those involving the Central Intelligence Agency.64

Intelligence agencies are exempt from reporting their contract obligations to FPDS-NG.65These agencies don’t disclose much other information, either. While overall budget figures for these two components are disclosed and are included in our tally of Pentagon spending, all other details about the budget are kept secret. For example, when the National Intelligence Program revealed that its 2024 budget was $76.5 billion, it provided no further details about how much went to contracts or other purposes. As the National Intelligence Program press release stated, “Beyond the disclosure of the National Intelligence Program top-line figure, there will be no other disclosures of currently classified National Intelligence Program budget information.”66Similarly, the Military Intelligence Program’s press release announcing its $29.8 billion 2024 budget said, “No other MIP budget figures or program details will be released, as they remain classified for national security reasons.”67

Secret intelligence contracts mean that there are actually far more Pentagon contract awards than are disclosed to the public through USAspending. This, in turn, opens up the possibility that the share of Pentagon spending obligated to contracts from 2020–2024 is higher than 54%, because most intelligence funding originates in — and counts toward — the Pentagon budget. Removing intelligence funding from the equation drives the contract share up to 61%:

Controlling for classified funding nets a seven percentage-point change to the estimated 54% share of Pentagon spending obligated to contracts. This change could be overstated because it assumes all — rather than just most — intelligence funding comes from the Pentagon budget. Conversely, this seven-point shift could also understate the effect of unreported secret contracts. In 2007, Salon reported that 70 % of the intelligence budget went to contractors, a figure confirmed by a press officer from the Directorate of National Intelligence.68

Foreign military sales

Not all Pentagon contracts listed by USAspending are funded by the Pentagon. Foreign Military Sales are a category of arms sales brokered by the U.S. government, executed through the Pentagon’s normal acquisition channels, and therefore are included in USAspending’s tally of Pentagon contracts, even though the foreign funding involved doesn’t count toward the Pentagon budget.

U.S. arms sales are conducted through one of two processes: Foreign Military Sales or Direct Commercial Sales. The latter are negotiated directly between a U.S. company and a foreign government. For the former, the U.S. government acts as a broker. Because of this, Foreign Military Sales are processed through the Pentagon’s normal acquisition channels, even though they involve foreign funding. That funding does not count toward the Pentagon’s budget, but the contracts funded by it count toward its contract obligations.

In its full dataset on Pentagon contracts,69USAspending indicates whether a given obligation is linked to a Foreign Military Sales.70Excluding these obligations reduces the share of military spending on contracts between fiscal years 2020 and 2024 from 54 to 48%.71

This six percentage-point shift assumes all Foreign Military Sales are paid in full by other countries, but that is not the case. Initially, we expected to use this 48 % figure as the lower bound of an estimated range. However, when we looked at the individual details of several of the largest Foreign Military Sales-labeled contracts, we noticed many of them are funded in part, and sometimes in full, by the Pentagon. A few examples are listed below.

For example, the largest Foreign Military Sales contract obligation in 2024, according to USAspending data, was $2.4 billion — part of a $3.2 billion award to Lockheed Martin on September 27, 2024, for anti-ship and air-to-surface missiles.72Sixty-nine percent ($1.7 billion) of the transaction was funded by the following accounts in the Pentagon’s 2024 budget: Air Force missile procurement ($1.5 billion), Navy weapon procurement ($176 million), and Air Force operation and maintenance ($2 million).73

The second-largest reported Foreign Military Sales contract obligation in 2024 was a $1.5 billion contract modification awarded to Northrop Grumman on July 19 for nine E-2 aircraft.74While this obligation, like the one above, is coded as a Foreign Military Sale in USAspending data, four of the nine aircraft procured are for the U.S. (with the remaining five for the government of Japan). Accordingly, nearly half the obligated amount ($689 million) was provided by the U.S. Navy aircraft procurement account.75

There are also instances of Foreign Military Sales paid for entirely by the U.S. On November 30, 2022, the Pentagon awarded a $1.2 billion contract to Raytheon for six National Advanced Surface-to-Air Missile Systems “in support of the efforts in Ukraine.”76The first tranche ($559 million) was obligated the same day,77and coded as a Foreign Military Sale in USAspending data. While the contract presumably followed the Foreign Military Sale procurement process and delivered weapons to a foreign country, no foreign funding was involved.78As the contract announcement makes clear, the missile systems were funded entirely by the Ukraine Security Assistance Initiative, a military aid program within the Pentagon’s operation and maintenance account.79

Offsetting effects

Adjusting to account for both factors produces the same result as the original: from 2020–2024, 54% of Pentagon spending was obligated to contracts. Below is a comparison of the original formula with one that accounts for arms sales and secret programs.

Original:

Accounting for arms sales and classified funding:

Related

Program

Entities

Authors

William D. Hartung is a senior research fellow at the Quincy Institute for Responsible Statecraft and an expert on the arms trade, Pentagon spending and strategy, and nuclear weapons policy. His books include The Trillion Dollar War Machine, and Prophets…

Stephen Semler is co-founder of Security Policy Reform Institute (SPRI), a think tank that works to align U.S. foreign policy with working-class interests. He also writes Polygraph, a data journalism newsletter

Citations

Figures in constant FY2025 dollars and refer to discretionary spending. Calculated from the General Services Administration (SAM.gov), Treasury Department (USASpending.gov), Office of Management and Budget, accessed April 2, 2025. Most military spending is discretionary. A very small amount (less than 2%) is mandatory spending, which is controlled by laws other than appropriations acts and primarily funds retirement benefits. Mann, Christopher. (2017, March 17). Defense Primer: The National Defense Budget Function (050). Congressional Research Service. https://www.congress.gov/crs-product/IF10618 ↩

There may be slight discrepancies in adding totals because of choices made in rounding numbers. ↩

$356 billion is the total, adding 2020-2024, spending on the annual “Department of State, Foreign Operations, and Related Programs” legislation, which funds the State Department, USAID, and most international assistance programs. Figures in constant 2025 dollars, adjusted using GDP deflator. Calculation based on combined funding for Titles I, II, III, V, and VI in annual SFOPS appropriations for fiscal years 20–24. ↩

U.S. Department of State, Bureau of Political-Military Affairs. (2025, March 12). Security Assistance to Ukraine. https://www.state.gov/bureau-of-political-military-affairs/releases/2025/01/u-s-security-cooperation-with-ukraine ; Bilmes, L., Hartung, W., & Semler, S. (2024, October 7). United States Spending on Israeli Military Operations and Related U.S. Operations in the Region, October 7, 2023 to September 30, 2024. Costs of War, Watson Institute, Brown University. https://watson.brown.edu/costsofwar/papers/2024/USspendingIsrael ↩

Congress.gov. FY2025 Defense Appropriations: Summary of Funding. (2025, June 20). https://www.congress.gov/crs-product/IN12425 ↩

Constant dollars are adjusted values that refer to the purchasing power of a dollar in a given year. By controlling for inflation, they are useful in comparing amounts over time. ↩

For an overview of discretionary spending, see this helpful infographic. Congressional Budget Office. (2025, March 20). Discretionary Spending in Fiscal Year 2024: An Infographic. https://www.cbo.gov/publication/61184. ↩

The federal budget function classification system examines spending by category rather than department. Budget Function 050 is frequently used to describe U.S. military spending levels. The Pentagon’s budget (Budget Subfunction 051) makes up more than 95% of discretionary military spending. Mann, C. (2017, March 17). Defense Primer: The National Defense Budget Function (050). Congressional Research Service. https://www.congress.gov/crs-product/IF10618 ↩

Congressional Budget Office analyses of H.R. 1968 and H.R. 10545. (2025). H.R. 1969, Full-Year Continuing Appropriations and Extensions Act, 2025. Congressional Budget Office, Cost Estimate. https://www.cbo.gov/system/files/2025-03/hr1968.pdf ↩

Congress.gov. (2025, July 4). H.R.1 – One Big Beautiful Bill Act. https://www.congress.gov/bill/119th-congress/house-bill/1/text ↩

Congressional Budget Office. (2025, June 29). Estimated Budgetary Effects of an Amendment in the Nature of a Substitute to H.R.1, the One Big Beautiful Bill Act, Relative to CBO’s January 2025 Baseline. https://www.cbo.gov/publication/61534 ↩

Hartung, W. (2021, September 13). Profits of War: Corporate Beneficiaries of the Post-9/11 Pentagon Spending Surge. Costs of War, Watson Institute, Brown University. https://watson.brown.edu/costsofwar/papers/2021/ProfitsOfWar. ↩

Semler, S. (2021, August 23). The Top Five Contractors Ate $2 Trillion During the Afghanistan War. Speaking Security. https://www.stephensemler.com/p/the-top-5-military-contractors-ate ↩

Officially classified as “Budget Subfunction 051,” which makes up over 95% of all funding under Function 050, mentioned above. ↩

Slight year-to-year variations can occur due to changes in how Congress writes the annual military spending legislation, what (if any) additional military spending legislation Congress passes, fluctuations in government-brokered arms sales (discussed in Appendix B), lag times in data reporting (likely affecting the most recent year shown on Figure 1, 2024), and other factors. ↩

Based on author analysis of Title II—One Big Beautiful Bill Act (https://www.congress.gov/bill/119th-congress/house-bill/1/text ) and previously-enacted appropriations (https://www.congress.gov/crs-product/IN12425). ↩

Because the Trump administration has stated it will begin obligating some of these funds only in the subsequent fiscal year, 2026, it is difficult at this stage to calculate an exact amount of the Pentagon’s 2025 budget predicted to go to contractors. However, the 54% figure suggests it will almost certainly be over $500 billion. ↩See footnote 3 for an explanation of this calculation. ↩

There may be slight discrepancies in totals due to choices made in rounding numbers. ↩

Gonzalez, R. (2024, April 17). How Big Tech and Silicon Valley Are Transforming the Military-Industrial Complex. Costs of War, Watson Institute, Brown University. https://watson.brown.edu/costsofwar/papers/2024/SiliconValley ↩

Edwards, J. (2025, March 10). Anduril $642 Million Navy Contract for Counter-Drone Tech. Govconwire, https://www.govconwire.com/2025/03/anduril-navy-contract-counter-drone-tech/; Albon, C. (2024, October 8).Anduril Lands $250 Million Pentagon Contract for Drone Defense System. Defense News. https://www.defensenews.com/unmanned/2024/10/08/anduril-lands-250-million-pentagon-contract-for-drone-defense-system/ ; ANDURIL. (2024, August 14). Anduril Australia to Build to Build Ghost Shark Factory. Anduril press release. https://www.anduril.com/article/anduril-australia-to-build-ghost-shark-factory/ ↩

Capaccio, A. (2025, February 11). Drone Maker Anduril to Take Over Managing Microsoft Goggles for US Army. Bloomberg. https://www.bloomberg.com/news/articles/2025-02-11/anduril-to-take-over-managing-microsoft-goggles-for-us-infantry ↩

Losey, S. (2025, March 21). Boeing Wins Contract for NGAD Fighter Jet, Dubbed F-47. Defense News. https://www.defensenews.com/air/2025/03/21/boeing-wins-contract-for-ngad-fighter-jet-dubbed-f-47/ ↩

Palantir. (2024, December 18). Palantir Expands Army Vantage Partnership with $618.9 Million Contract. Palantir press release. https://investors.palantir.com/news-details/2024/Palantir-Expands-Army-Vantage-Partnership-with-618.9M-Contract/ ; U.S. Department of Defense. Contracts for May 29, 2024. https://www.defense.gov/News/Contracts/Contract/Article/3790490/ ; U.S. Department of Defense. ↩

Dou, E. & Gregg, A. (2024, December 7). Elon Musk’s Martian Dreams are a Boon to the U.S. Military. The Washington Post. https://www.washingtonpost.com/technology/2024/12/07/musk-mars-technology-us-national-security/ ↩

González, R. (2024, April 17). How Big Tech and Silicon Valley Are Transforming the Military-Industrial Complex. Costs of War, Watson Institute, Brown University. https://watson.brown.edu/costsofwar/papers/2024/SiliconValley ↩

Anduril. Rebooting the Arsenal of Democracy: Anduril Mission Document. Accessed March 17, 2025. https://www.anduril.com/article/rebooting-the-arsenal-of-democracy-anduril-mission-document/ ↩

Grazier, D. (2024, February 26). F-35: The Part-Time Fighter Jet. Project on Government Oversight. https://www.pogo.org/analysis/f-35-the-part-time-fighter-jet; Copp, T. (2024, July 9). New Sentinel Nuclear Weapons Program is 81% Over Budget. But Pentagon Says It Must Go Forward. Associated Press. https://apnews.com/article/nuclear-sentinel-weapon-icbm-cost-39c69242301b2a273111d161573f5c56 ; Van Allen, F. (2019, December 10). Meet the Military’s $13 Billion Aircraft Carrier. CNET. https://www.cnet.com/pictures/meet-the-navys-new-13-billion-aircraft-carrie ; Sapien J. (2023, September 7). The Inside Story of How the Navy Spent Billions on the ‘Little Crappy Ship. ProPublica. https://www.propublica.org/article/how-navy-spent-billions-littoral-combat-ship ↩

Hambling, D. (2024, November 26). Musk Calls F-35 Builders ‘Idiots,’ Favors Drone Swarms. Forbes. https://www.forbes.com/sites/davidhambling/2024/11/26/elon-musk-calls-f-35-builders-idiots-favors-drone-swarms/ ↩

González, R. (2024, April 17). How Big Tech and Silicon Valley Are Transforming the Military-Industrial Complex. Costs of War, Watson Institute, Brown University. https://watson.brown.edu/costsofwar/papers/2024/SiliconValley ↩

Forum on the Arms Trade. Major Arms Sales Notification Tracker. Accessed June 2025. https://www.forumarmstrade.org/major-arms-sales-notifications-tracker.html ↩

U.S. Department of State. (2025, March 12). U.S. Security Cooperation with Ukraine. https://www.state.gov/bureau-of-political-military-affairs/releases/2025/01/u-s-security-cooperation-with-ukraine ↩

Bilmes, L., Hartung, W., & Semler, S. (2024, October 7). United States Spending on Military’s Military Operations and Related U.S. Operations in the Region, October 7, 2023 to September 26, 2024. Costs of War, Watson Institute, Brown University. https://watson.brown.edu/costsofwar/papers/2024/USspendingIsrael ↩

Tucker, P. (2023, October 19). ‘Arsenal of Democracy’ – Biden Asks Congress to Boost Aid to Ukraine, Israel. Defense One. https://www.defenseone.com/policy/2023/10/arsenal-democracy-biden-pitches-congress-more-weapons-ukraine-and-israel/391374/ ↩

Calculation by Ashley Gate of the Quincy Institute, based on data supplied by the Stockholm International Research Institute and the annual tally of conflicts put together by the Armed Conflict Location and Event Data project (ACLED), at https://acleddata.com/conflict-index/; and Freedom House data set on global freedom, accessed March 18, 2025. https://freedomhouse.org/countries/freedom-world/scores ↩

Semler, S. (2023, May 11). Biden Is Selling Weapons to the Majority of the World’s Autocracies. The Intercept. https://theintercept.com/2023/05/11/united-states-foreign-weapons-sales/ ↩

George, M., Djokic, K., Hussain, Z., Wezeman, P., & Wezeman, S, (2025, March). Trends in International Arms Transfers, 2024. Stockholm International Peace Research Institute. https://www.sipri.org/sites/default/files/2025-03/fs_2503_at_2024_0.pdf ↩

Open Secrets. Defense Sector Summary. Accessed March 17, 2025. https://www.opensecrets.org/industries/indus?Ind=D ; Think Tank Funding Tracker, accessed March 17, 2025. https://thinktankfundingtracker.org/ ; Tiron, R. (2025, January 13). GOP Defense Leaders Pushing Trillion-Dollar Pentagon Budget. Bloomberg.. https://news.bgov.com/bloomberg-government-news/boosting-defense-spending-is-top-goal-for-armed-services-leaders ↩

OpenSecrets. Lobbying Profile: Defense. Accessed April 3, 2025. https://www.opensecrets.org/federal-lobbying/sectors/summary?id=D ↩

Lipton, E. (2023, December 30). New Spin on a Revolving Door: Pentagon Officials Turned Venture Capitalists. The New York Times. https://www.nytimes.com/2023/12/30/us/politics/pentagon-venture-capitalists.html ↩

Lipton, E. (2023, December 30). ↩

Freeman, B. & Cleveland-Stout, N. (2025, January 3). Big Ideas and Big Money: Think Tank Funding in America. Quincy Institute for Responsible Statecraft. https://quincyinst.org/research/big-ideas-and-big-money-think-tank-funding-in-america/#executive-summary ↩

Reif, K. & Sanders-Zakre, A, (2019, April). U.S. Nuclear Excess: Understanding the Costs, Risks, and Alternatives. Arms Control Association. https://www.armscontrol.org/sites/default/files/files/Reports/Report_NuclearExcess2019_update0410_0.pdf ↩

Grazier, D. (2018, December 10). Panel of Defense Lobbyists and Revolving Door Doyens Calls for More Defense Spending, Project on Government Oversight. https://www.pogo.org/analysis/panel-of-defense-lobbyists-and-revolving-door-doyens-calls-for-more-defense-spending ↩

Copp, T. (2025, March 21). Eyeing China Threat, Trump Announces Boeing Wins Contract for Secretive Future Fighter Jet. Associated Press. https://apnews.com/article/fighter-jet-ngad-trump-hegseth-china-55d7b3d15e5a4fa9cb061ec85ac19ae2 ↩

Cohen, Z. & Liebermann, O. (2025, March 22). Trump Wants a Golden Dome Capable of Defending the Entire U.S. – ‘Strategically, it doesn’t make any sense. CNN.com. https://www.cnn.com/2025/03/22/politics/pentagon-golden-dome-scramble/index.html ↩

Hartung, W. (2025, January 25). High Tech Militarists are Hijacking the Trump Administration. The Nation. https://www.thenation.com/article/politics/elon-musk-doge-trump-silicon-valley-oligarchs/ ↩

Pabst, S. (2025, March 13). Another Weapons Industry Exec Brought Into Trump’s Pentagon. Responsible Statecraft. https://responsiblestatecraft.org/michael-obadal-trump/ ↩

Alexander, S. & Taraby, J. (2025, March 7). Peter Thiel’s Deep Ties to Pentagon Top Ranks. Bloomberg. https://www.bloomberg.com/features/2025-peter-thiel-trump-administration-connections/ ↩

Brenes, M. & Hartung, W. (2024, June). Private Finance and the Quest to Remake Modern Warfare. Quincy Institute for Responsible Statecraft, Quincy Brief Number 57, pp. 5-10. https://quincyinst-2.s3.amazonaws.com/wp-content/uploads/2024/06/31124329/QUINCY-BRIEF-NO.-57-JUNE-2024-BRENES-HARTUNG-1.pdf ↩

Hartung, W. (2025, January 25). High Tech Militarists are Hijacking the Trump Administration. The Nation. https://www.thenation.com/article/politics/elon-musk-doge-trump-silicon-valley-oligarchs/ ↩

Data in this section comes from the most recent annual report of each of the listed companies, which cover developments through 2023. ↩

Specifically, we divided the Pentagon’s contract obligations — obligations being binding agreements that result in immediate or future spending — by its total obligation authority, an internal financial metric that reflects how much money the department can legally obligate in a given year, whether for contracts or other purposes. Because the Pentagon has not yet released its finalized TOA for 2024, the department’s discretionary budget authority is used in its place for that fiscal year. Budget authority is the amount provided by law to enter into obligations. This should not have a significant effect on our estimates — in recent years, there has been little difference between TOA and discretionary budget authority. DAU. Budget Authority. https://www.dau.edu/glossary/budget-authority; Congressional Budget Office. (2024, November). Long-Term Implications of the 2025 Future Years Defense Program. https://www.cbo.gov/system/files/2024-11/60665-FYDP25.pdf#page=4; DAU. Obligation.; https://www.dau.edu/glossary/obligation ; DAU. Total Obligation Authority. https://www.dau.edu/glossary/total-obligation-authority ↩

USAspending.gov. Award Data Archive. https://www.usaspending.gov/download_center/award_data_archive ↩

All values refer to Budget Subfunction 051 — a subset of Budget Function 050 that refers to military spending strictly in the Pentagon’s departmental discretionary budget — and were converted into constant dollars using the Office of Management and Budget’s GDP deflator, re-baselined to 2025. National Defense Budget Estimates for FY2025. Office of the Under Secretary of Defense (Comptroller). U.S. Department of Defense. pp.54. https://comptroller.defense.gov/Portals/45/Documents/defbudget/FY2025/fy25_Green_Book.pdf#page=61 ↩

USAspending.gov. Data Sources. https://www.usaspending.gov/data-sources ↩

Federal Acquisition Regulation. 48 CFR § 4.606(c)(5). https://www.acquisition.gov/far/part-4#FAR_4_606 ↩

Federal Acquisition Regulation. 48 CFR § 4.606(c)(6). https://www.acquisition.gov/far/part-4#FAR_4_606 ↩

Congressional Research Service. (2025, March 14). Defense Primer: Department of Defense Classified Funding. https://www.congress.gov/crs_external_products/IF/PDF/IF12943/IF12943.2.pdf#page=1 ↩

United States Government Accountability Office. Report to Congressional Committees. (2012, January). DEFENSE CONTRACTING: Improved Policies Tools Could Help Increase Competition on DOD’s National Security Exception Procurements. https://www.gao.gov/assets/gao-12-263.pdf#page=16 ↩

Congressional Research Service. (2024, September 24). Intelligence Community Spending Trends. https://sgp.fas.org/crs/intel/R44381.pdf#page=8 ↩

Congressional Research Service. (2025, March 14). Defense Primer: Department of Defense Classified Funding. https://www.congress.gov/crs_external_products/IF/PDF/IF12943/IF12943.2.pdf#page=1 ↩

Congressional Research Service. (2024, September 26). Intelligence Community Spending Trends. https://sgp.fas.org/crs/intel/R44381.pdf#page=8 ↩

Congressional Research Service. (2025, March 14). Defense Primer: Department of Defense Classified Funding. https://www.congress.gov/crs_external_products/IF/PDF/IF12943/IF12943.2.pdf#page=1 ↩

United States Government Accountability Office: Report to Congressional Request. (2014, June). DATA TRANSPARENCY: Oversight Needed to Address Underreporting and Inconsistences on Federal Award Website. https://www.gao.gov/assets/gao-14-476.pdf#page=16 ↩

Office of the Director of National Intelligence. (2024, October 31). DNI Releases Appropriated Budget Figure for 2024 National Intelligence Program. Press Release. https://www.dni.gov/index.php/newsroom/press-releases/press-releases-2024/4013-pr-27-24 ↩

U.S. Department of Defense. (2024, October 31). Department of Defense Releases Fiscal Year 2024 Military Intelligence Program Budget. https://www.defense.gov/News/Releases/Release/Article/3952746/department-of-defense-releases-fiscal-year-2024-military-intelligence-program-b/ ↩

Shorrock, T. (2007, June 1). The corporate takeover of U.S. intelligence. Salon. https://www.salon.com/2007/06/01/intel_contractors/ ↩

USAspending.gov. Award Data Archive. https://www.usaspending.gov/download_center/award_data_archive ↩

Starting in 2012, the Federal Procurement Data System — from which USAspending draws its contract data — began identifying contracts with FMS funding. Acquisition Research Program. (2022, May 11-12). Excerpt from the Proceedings of the Nineteenth Annual Acquisition Research Symposium. Acquisition Research: Creating Synergy for Informed Change. https://dair.nps.edu/bitstream/123456789/4575/1/SYM-AM-22-062.pdf#page=4 ↩

Contract obligations (in FY2025 dollars) fall by $2.4 trillion to $2.1 trillion, respectively. ↩

U.S. Department of Defense. Contracts For Sept. 27, 2024. Air Force. Contract FA868224CB001. Defense.gov. https://www.defense.gov/News/Contracts/Contract/Article/3919852/ ↩

USAspending.gov. Definitive Contract. https://www.usaspending.gov/award/CONT_AWD_FA868224CB001_9700_-NONE-_-NONE- ↩

U.S. Department of Defense. Contracts For July 19, 2024. Navy. Defense.gov. Modification P00086 to contract N0001918C1037. https://www.defense.gov/News/Contracts/Contract/Article/3844604/ ↩

USAspending.gov. Definitive Contract. https://www.usaspending.gov/award/CONT_AWD_N0001918C1037_9700_-NONE-_-NONE-/ ↩

Contract W31P4Q-23-C-0002. U.S. Department of Defense. Contracts for November 30, 2022. Defense.gov. https://www.defense.gov/News/Contracts/Contract/Article/3232469/ ↩

USAspending.gov. (n.d.). Contract W31P4Q23C0002. Retrieved April 15, 2025. https://www.usaspending.gov/award/CONT_AWD_W31P4Q23C0002_9700_-NONE-_-NONE- ↩

U.S. Army. (2022, November 30). Army announces contract award for National Advanced Surface to Air Missile Systems. Army.mil. https://www.army.mil/article/262383 ↩

U.S. Department of Defense. (2022, November 30). Contracts for November 30, 2022. Defense.gov. https://www.defense.gov/News/Contracts/Contract/Article/3232469/ ↩