The Fiscal Implications of a Major Increase in U.S. Military Spending

Executive Summary

A growing number of influential Washington commentators are calling for a massive increase in military spending. For example, Republican Sen. Roger Wicker of Mississippi, the incoming chair of the Senate Armed Services Committee, supports a proposal to raise military spending to 5 percent of gross domestic product, GDP. This would increase annual defense spending by almost 90 percent in real (inflation-adjusted) terms. The congressionally mandated bipartisan Commission on the National Defense Strategy has called for military spending “commensurate with the national effort seen during the Cold War,” implying spending levels equivalent to perhaps 7 percent of GDP.

The case for such a dramatic increase in military spending is far from compelling — among other things, the United States already spends far more on defense than does China. Rather than focusing on the lack of need for such an increase, however, this paper examines the dangerous fiscal implications if that increase occurred. In brief, the paper finds:

- There is essentially no chance that any new defense spending buildup will be paid for through tax increases. Indeed, the new administration and Congress appear to be committed to implementing significant tax cuts.

- It is difficult to imagine implementing cuts to domestic programs that would come close to offsetting a massive increase in military spending. The proposed buildup would coincide with structural changes — particularly the rising share of America’s elderly population — that have created largely unavoidable pressures to increase spending on Social Security and, especially, major federal health care programs.

- Boosting military spending to 5 percent of GDP, without paying for it, would dramatically grow the federal debt. It would more than double, or, if combined with tax cuts, triple the size of the “fiscal gap” — a measure of the gap between spending and revenue that would need to be closed to stabilize the federal debt.

- Under current policies, the fiscal gap that would need to be closed, through tax increases and/or entitlement reform, to stabilize the federal debt is equivalent to about 1.5 percent of GDP. Although politically difficult, a deal of this magnitude is eminently doable. But a large military spending increase combined with a tax cut would turn the federal debt into a far more intractable problem.

It has become fashionable to claim that “deficits don’t matter.” But the massive growth in the debt burden that would result from an extreme military spending expansion would significantly increase the risks to the country’s long-term economic growth and its ability to respond to economic downturns, as well as exacerbate the potential for excessive borrowing to trigger a financial crisis. Congressional Budget Office models find that by the 2050s, uncontrolled growth in debt levels could create trillions of dollars in annual costs to the economy. In the end, such policies would do far more to damage than to enhance U.S. national security.

Introduction

Overview

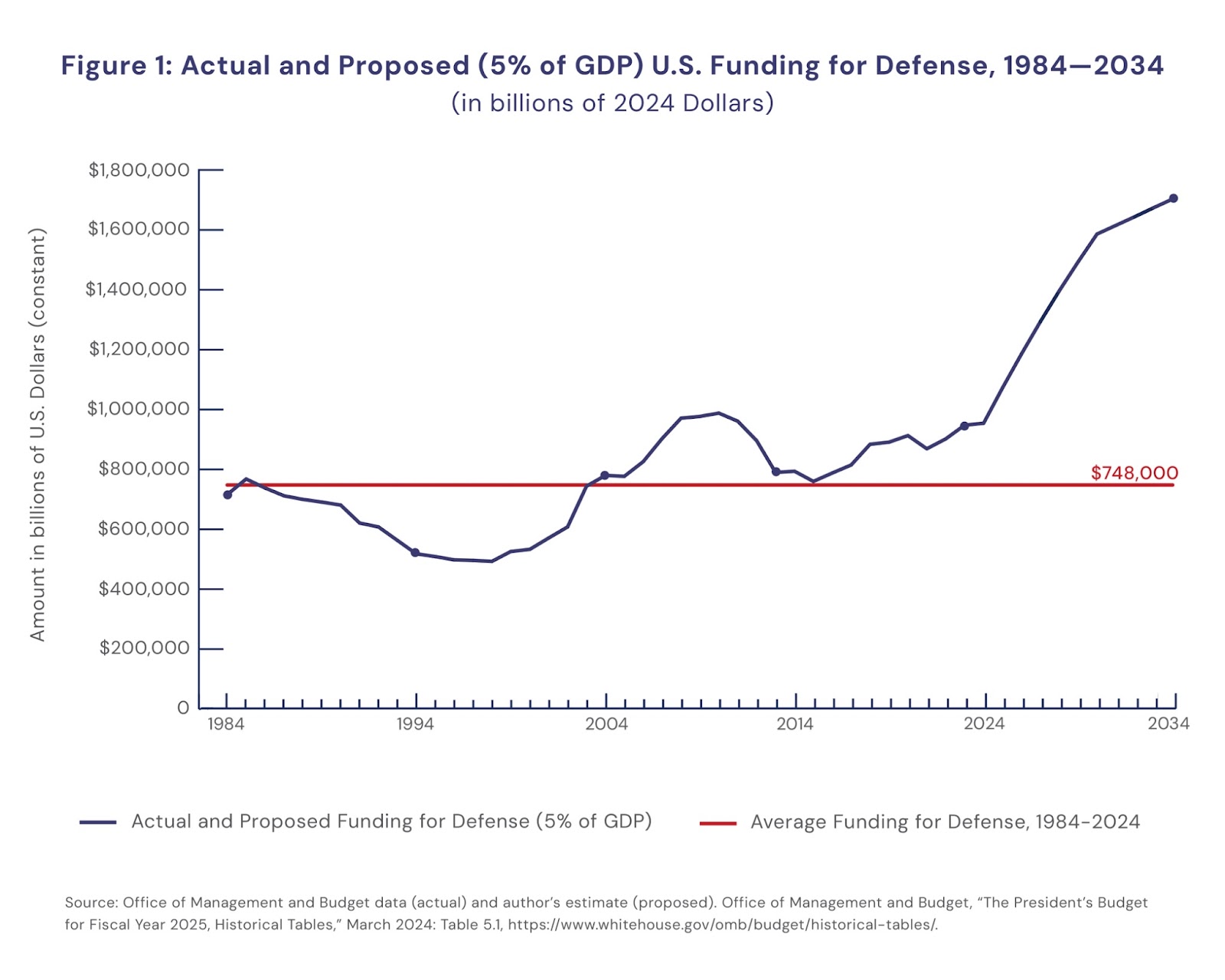

A rising chorus of politicians, think tank analysts, and defense industry representatives have in recent years called for a major increase in U.S. spending on defense. Under one well-publicized proposal, supported by Sen. Roger Wicker, the incoming chair of the U.S. Senate Armed Services Committee, and many others, the defense budget would be increased to a level equivalent to 5 percent of U.S. GDP.1This would boost annual spending on defense by some 88 percent in real (inflation-adjusted) terms to some $1.7 trillion by 2034.2It would bring U.S. defense spending to more than twice the average of the past 40 years — including the peak level reached during the Cold War — as measured in dollar terms. (See Figure 1.)

This paper uses the 5 percent of GDP benchmark advanced by Sen. Wicker and others as the baseline for its analysis of a major increase in U.S. defense spending. But it should be noted that other voices in Washington are calling for an even greater increase. Robert Wilkie, the head of the incoming Trump administration’s Pentagon transition team, has called for an increase in military spending to 6 percent of GDP.3And the congressionally mandated Commission on the National Defense Strategy has recently called for a military spending increase that would “support efforts commensurate with the U.S. national effort seen during the Cold War,” which, based on average military spending between 1946 and 1979, would imply spending greater than 7 percent of GDP.4These levels would make the fiscal implications outlined below even more extreme.

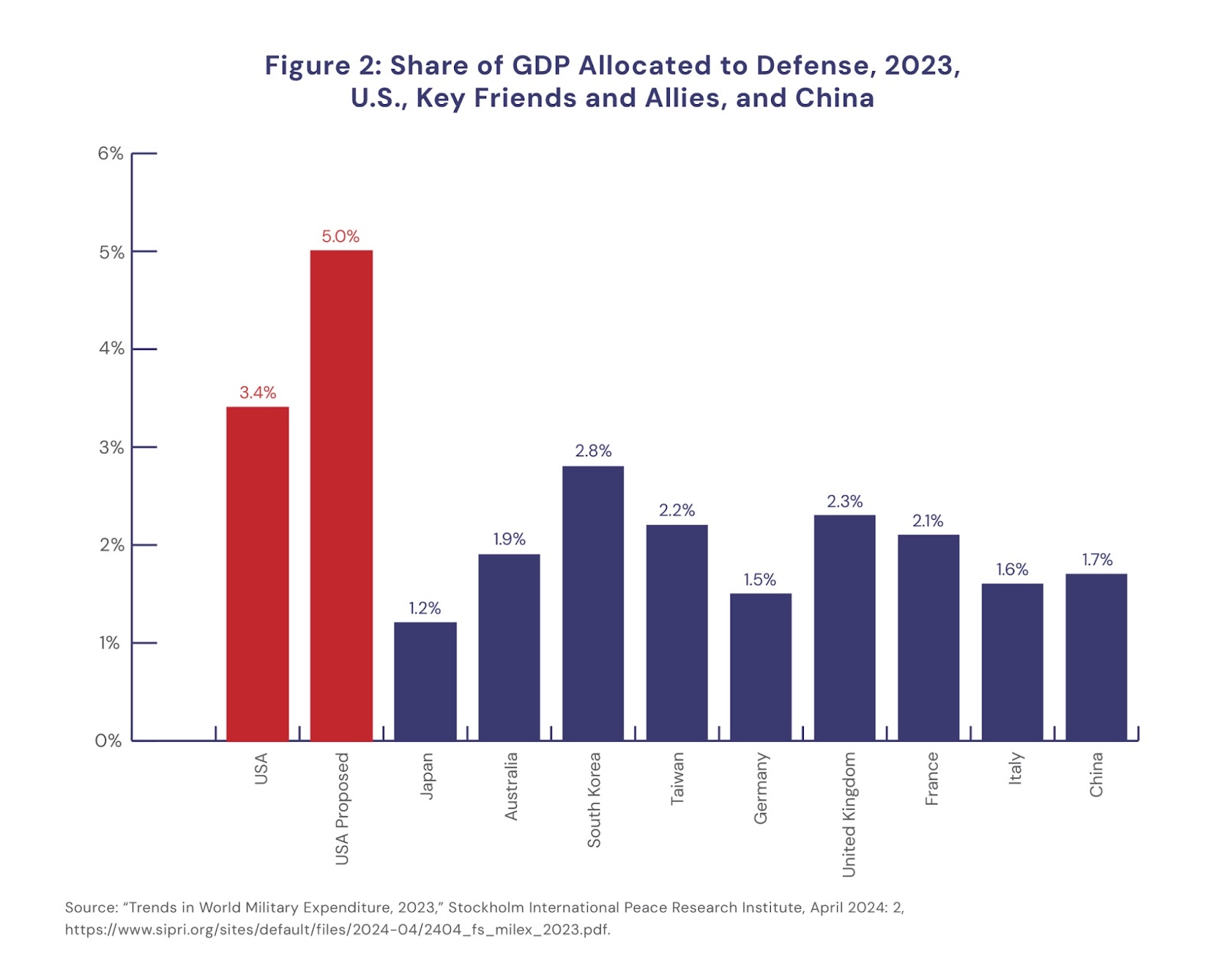

Such a large increase is unnecessary on national security grounds. As previous reports for the Quincy Institute have argued persuasively elsewhere, current levels of defense spending are more than adequate to meet key U.S. national security requirements, and exceed what would be needed were the United States to adopt a more restrained approach to its security.5The United States already spends far more on defense than China does, and enjoys an advantage in defense spending well in excess of what it did over the Soviet Union during the Cold War.6Moreover, as a share of their economies, the proposed level of spending would also exceed what U.S. allies and friends in both Europe and East Asia — the countries the U.S. military is largely intended to help defend — spend on their own militaries, or even what China spends. (See Figure 2.)

But worse than simply being unnecessary, such a large increase in defense spending would have severely negative consequences for U.S. security over the long run. This is because those calling for this enormous increase in defense spending have offered no realistic way of paying for it — either through tax increases or programmatic cuts to other parts of the federal budget. This means that any such increase in defense spending would inevitably add to the already difficult challenge posed by a growing federal debt — specifically the danger such a debt poses to America’s economy and, ultimately, its ability to compete with China.7

Just how much the proposed increase in defense spending could exacerbate an already difficult situation can be seen in the impact such an increase in spending would have on America’s ability to stabilize the federal debt in coming years. Unfortunately, media coverage of the federal debt overwhelmingly tends to focus on its projected future growth rather than on the adjustments — mathematically significant but manageable — that would need to be made to stabilize the debt and keep the federal budget on a sustainable path. The “fiscal gap” — a measure of the projected gap between government programmatic spending and revenue that would need to be closed through tax increases, program cuts, or a combination of the two to stabilize the level of federal debt — is equivalent to about 1.5 percent of the U.S. economy.8Among other things, the significant but manageable size of this gap reflects the fact that federal programmatic or “primary” spending (i.e., spending exclusive of net interest), under current law and policies, is actually projected to grow only relatively modestly in coming decades.

An unpaid-for increase in defense spending of the magnitude noted above would, however, dramatically change this math. It would turn a politically difficult problem — but in budgetary terms, manageable and fixable — into a dramatically more dangerous challenge. Specifically, unless it is somehow paid for, the proposed increase in defense spending would more than double the size of the fiscal gap to some 3.7 percent of GDP.9Currently, there is no realistic prospect that such an increase in defense spending would be paid for.

The congressionally mandated Commission on the National Defense Strategy, which in 2024 called for significantly increasing defense spending, explicitly acknowledged that taxes would need to be raised to help pay for any sizable boost. Indeed, it noted that the higher defense spending levels (as a share of GDP) sustained during the Cold War were made possible in part by the willingness of the U.S. to maintain “top marginal income tax rates above 70 percent and corporate tax rates averaging 50 percent.”10In this acknowledgment of the need to raise taxes, however, the commission is very much the exception.

Far from proposing tax increases to offset even part of the proposed increase in defense spending, most advocates of a major boost in such spending — mirroring the history of past buildups — have instead called for simultaneously cutting taxes, particularly through an extension of the 2017 Trump administration tax cuts, which are set to expire at the end of 2025. As a candidate, Donald Trump signaled his support for increasing defense spending, but did not commit to a specific level. It is clear, however, that his administration and Republicans in Congress will put a high priority on enacting large tax cuts.

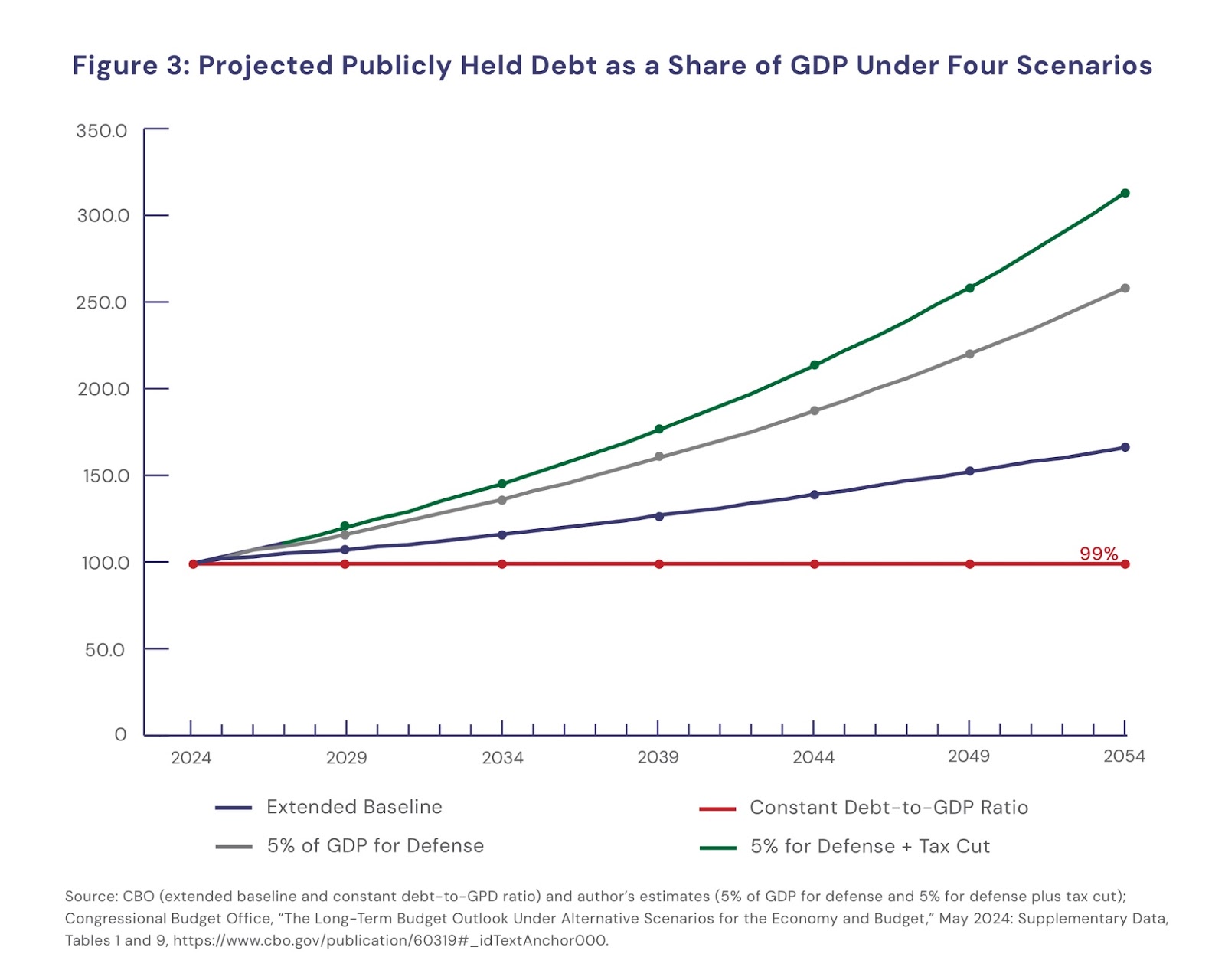

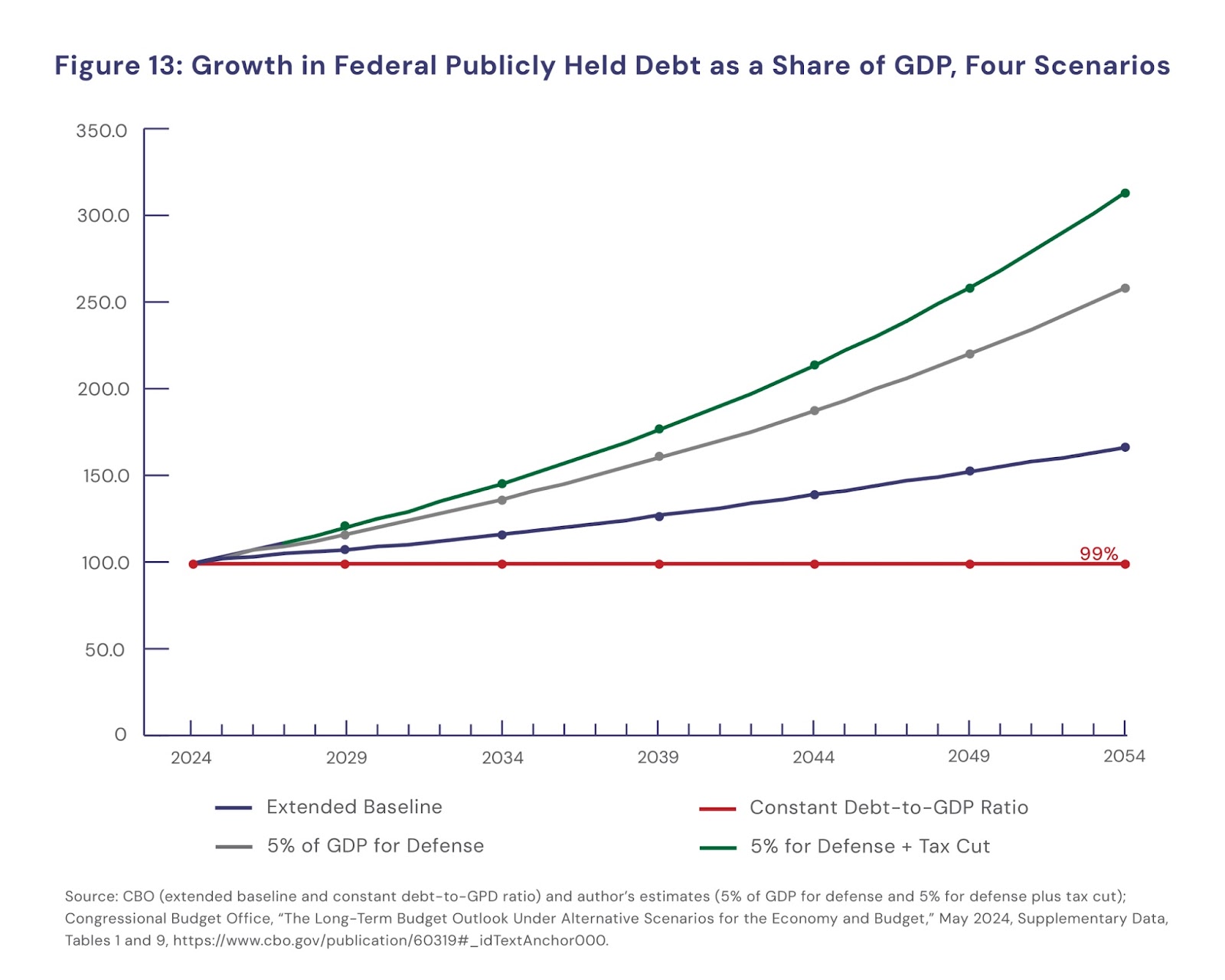

Combined, increasing defense spending to 5 percent of GDP and implementing a major tax cut could more than triple the size of the fiscal gap compared to currently projected levels. Under current law and policies, the debt is projected to grow from about 99 percent of GDP today to 166 percent of GDP by 2054, driven primarily by increasing interest payments.11If the proposed increase in defense spending were implemented and sustained (once implemented, there would be enormous pressure to sustain such an increase12), over the next three decades, the debt would grow to some 260 percent of GDP.13Worse yet, combined, implementing the proposed increases in defense spending and tax cuts could cause the debt to jump even higher, to some 310 percent of GDP by 2054.14(See Figure 3.)

The United States is a wealthy country, and it can carry a substantial level of debt without posing a significant risk to its financial stability or long-term economic growth. However, the growth of the federal debt along the lines described above would be far above current or historical levels and on anything but a stable and, thus, sustainable path. Concerns about a rising debt-to-GDP ratio include its effect on both long-term economic growth and the country’s ability to respond to significant economic downturns, inefficiencies associated with excessive borrowing, and the potential for such borrowing to trigger a financial crisis. An acceleration of the debt driven by a massive increase in defense spending, especially if combined with tax cuts, would greatly exacerbate each of these dangers. Indeed, it is difficult to imagine a weaker and more fragile economic, financial, and budgetary foundation upon which to rest the country’s long-term security — including, ultimately, its military capabilities — than the one that would be constructed under such a set of policies.

Many advocates of a large new buildup of the defense budget have called for offsetting those increases with spending reductions in other parts of the federal budget. However, with only very limited exceptions, these proposals have glibly and misleadingly assumed the generation of enormous savings in programmatic areas that, in practice, are either too small to realistically generate large savings, would involve cuts to other important national security related programs, or are highly resistant to cuts because they are too critical to too many Americans and, in key areas, are linked to long-projected changes in the country’s demographics.15

The purpose of this paper is to focus on this persistent misconception and, specifically, to dispel the simplistic — and for purposes of meaningfully addressing the country’s growing federal debt burden, counterproductive and unhelpful — notion that generating major reductions in other federal spending to pay for a large, sustained increase in defense spending is realistic. It isn’t.

This paper explores this topic by providing a primer on federal nondefense spending, including discretionary and mandatory spending. In its many details the federal budget is obviously complex. However, most federal spending actually comprises a surprisingly small number of major programs, the purposes of which are relatively easy to describe and understand. Understanding “where the money goes” makes it far clearer why so much of the federal budget would be so difficult to cut. This paper seeks to provide that understanding.

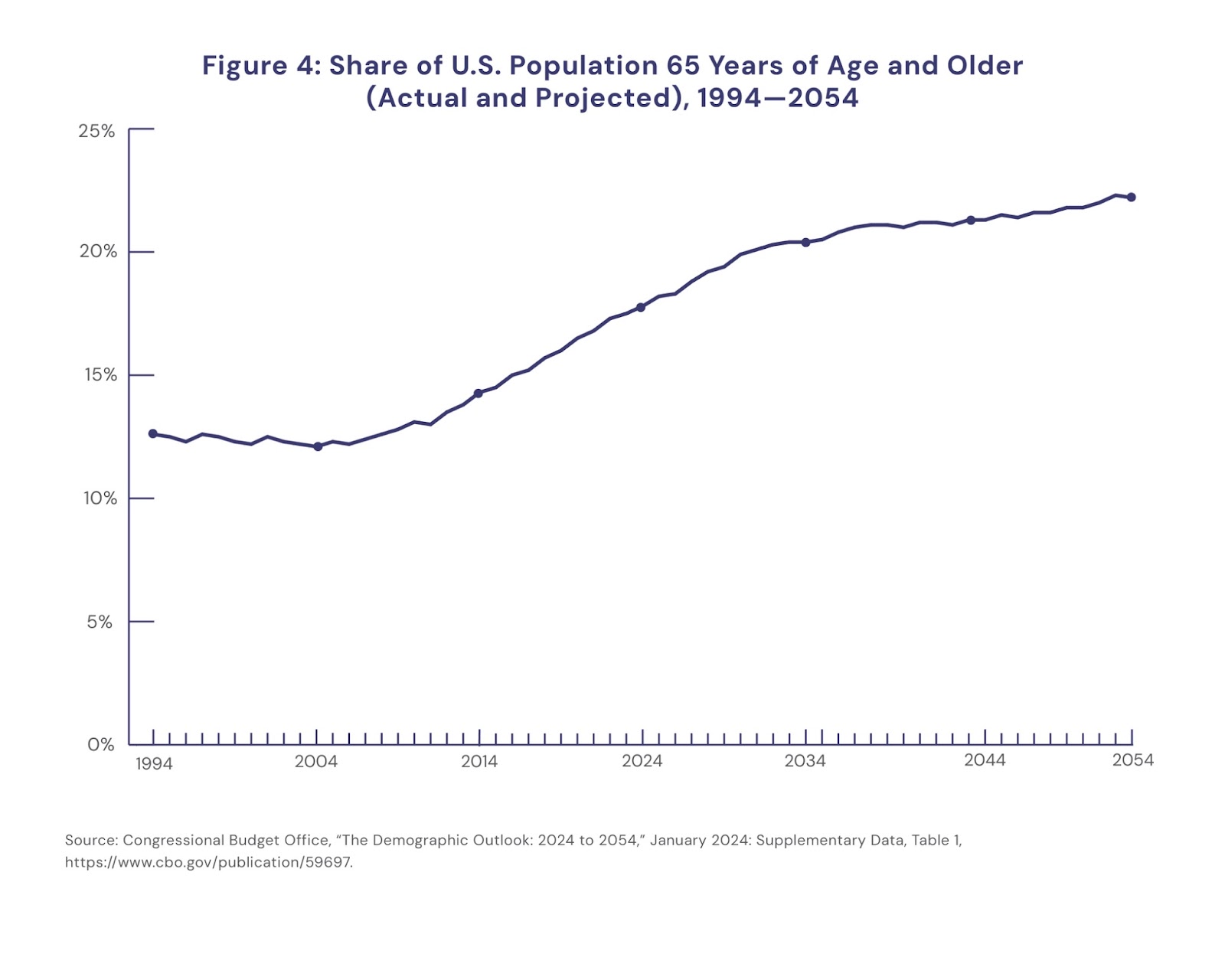

Absent such an understanding, there is a very real danger that, once again, the United States will embark on a defense spending buildup that will significantly add to federal deficits and the debt — as it has multiple times in the past. Increases in defense spending contributed greatly to the growth of the federal debt that occurred over the past two decades. But the impact would be far worse this time. This is because — much more so than in the past — the proposed new buildup would coincide with structural changes — particularly the rising share of America’s population that is elderly — that have created significant and largely unavoidable pressures to increase federal spending. In particular, these pressures will result in spending on Social Security, Medicare, and other major federal health care programs that is well above the levels of earlier periods, when the demographics of the country were fundamentally different. (See Figure 4.)

To be clear, this paper does not argue that America’s growing federal debt can be effectively addressed by, individually, restraining the growth of spending in areas outside of defense and national security, cuts or restraint in defense spending, or tax increases. As with each of the most effective past efforts at deficit reduction, any serious future effort to stabilize the federal debt is likely to include all three elements — restraining spending on defense, increasing taxes, and, at least within the limits allowed by America’s changing demographics, slowing the growth in spending on nondefense programs, including entitlements.

Rather, the argument of this paper is that current calls for embarking on a new increase in defense spending need to be weighed against the cost to America’s long-term security that such an increase would have on our federal debt burden. As stated, there is no realistic prospect that such an increase would come close to being paid for through cuts in nondefense spending. The consequences of such an unpaid-for defense buildup would be even more dangerous if combined with a major tax cut — a feature common to every major defense buildup since the 1980s. Claims that deep cuts in other areas of the federal budget will somehow materialize once we have boosted defense spending (and cut taxes) is, at best, dangerous, wishful thinking. At worst, they betray an equally dangerous view that further accelerating the growth of America’s debt burden isn’t something the U.S. need worry about.

Instead of a new round of unsustainable and unnecessary increases in defense spending, policymakers in Washington should be looking for ways to address the fiscal gap and stabilize U.S. debt. A budget agreement that stabilizes the federal debt is eminently doable — if the political will can be found — and is vital to sustaining America’s economic strength over the long run and, thereby, our national security. Such an outcome would do far more to secure America’s future than would a massive military expansion built on a fragile economic foundation. But such an agreement can come about only if policymakers and the American public have a realistic understanding of the federal budget — particularly the critical role federal programmatic spending plays in the lives of all Americans and the sources and magnitude of its projected growth.

Federal Budget: Where the Money Goes

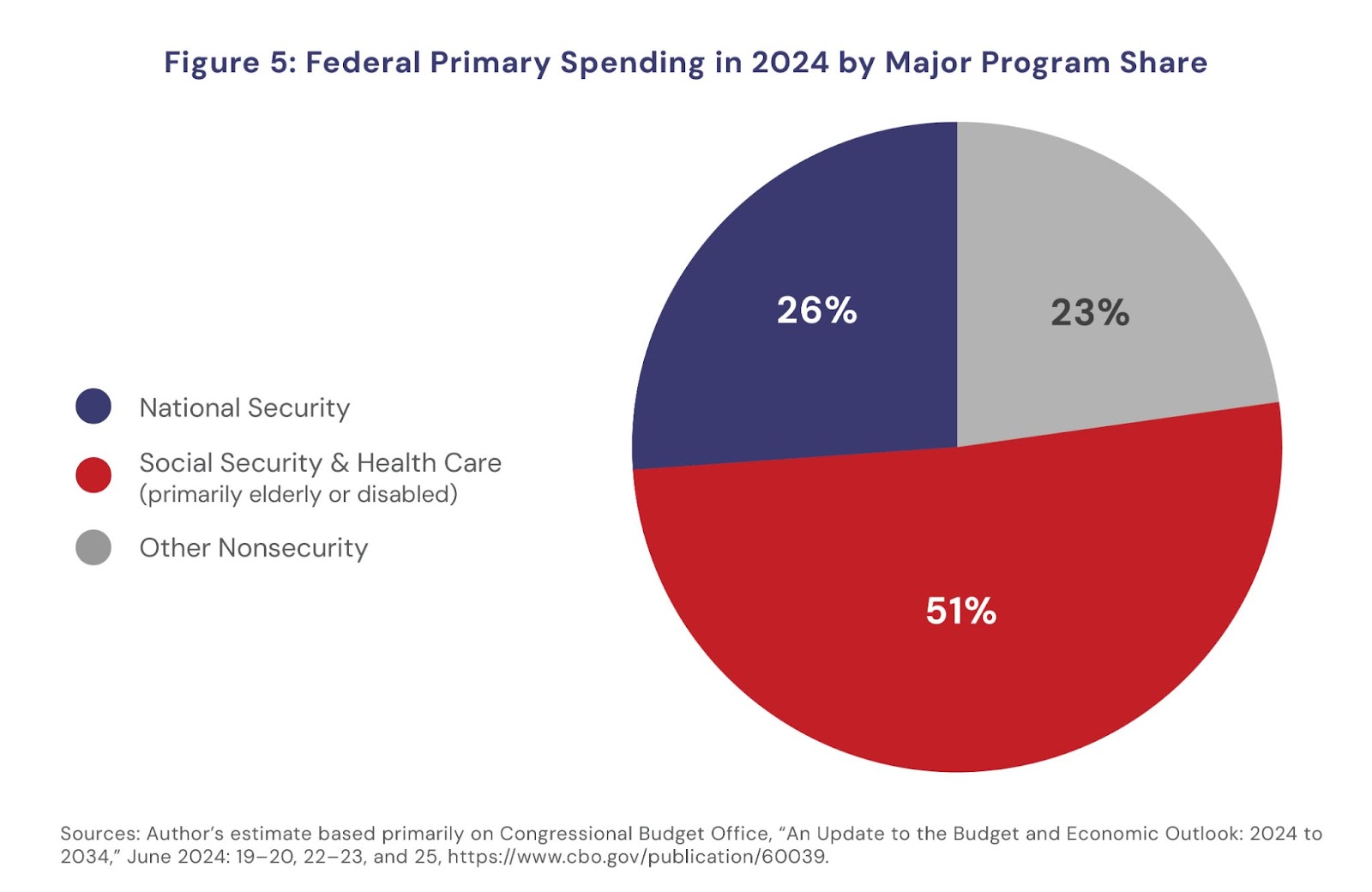

Federal spending is used to support a broad range of programs and activities, covered in thousands of line items in annual budget documents. However, the vast majority of federal spending fits within a handful of buckets, the focus and purposes of which are relatively well-defined. (See Figure 5.)

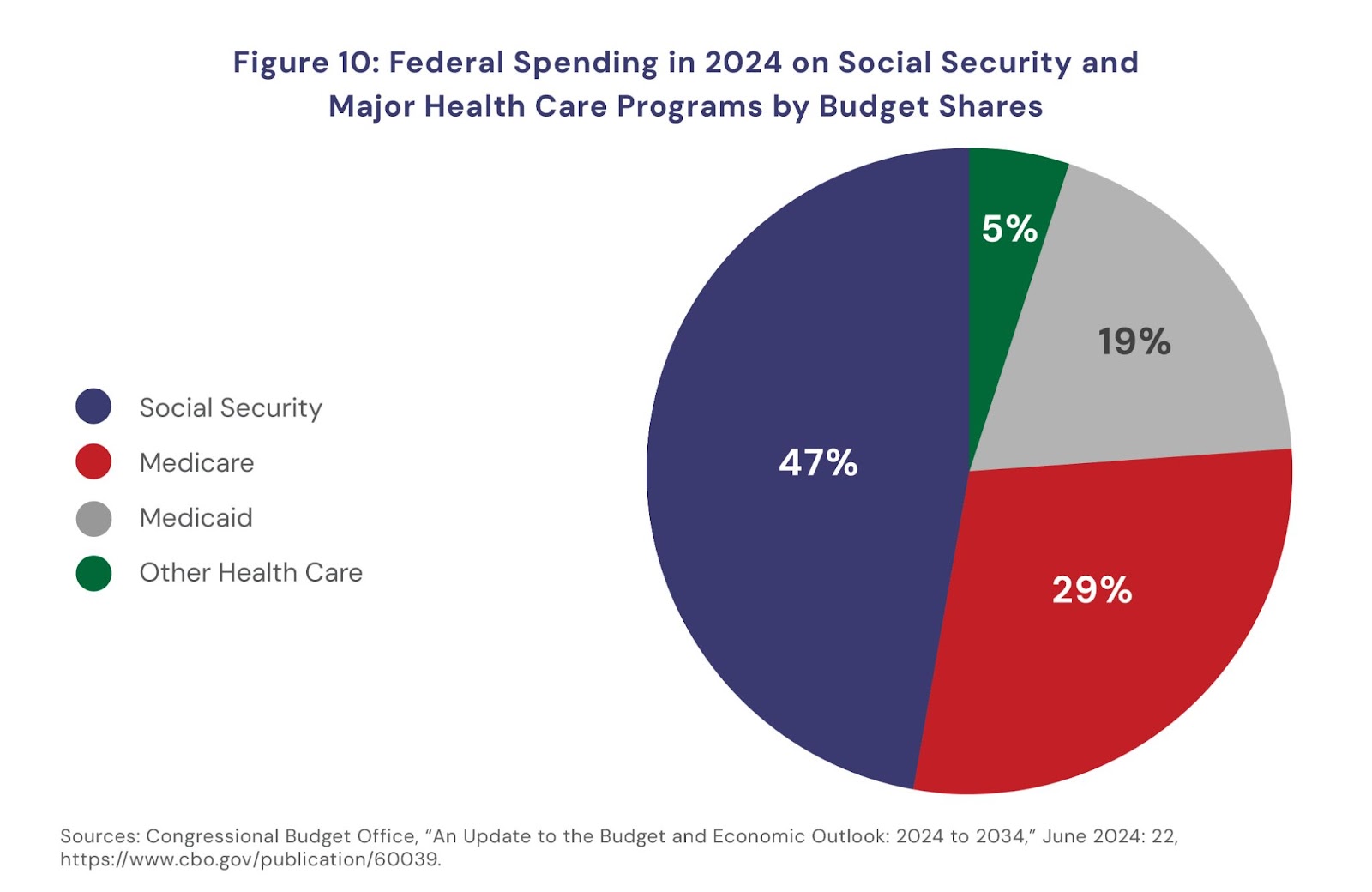

In the simplest terms, the federal government — in terms of its spending — can be described as an insurance company with a military. About half of federal programmatic or “primary” spending is used for Social Security and Medicare and other major health care programs. These programs provide, respectively, pensions and health insurance to their beneficiaries — much in the same way that private insurance companies provide retirement annuities, disability insurance, and health insurance. This spending is roughly equally divided between, on the one hand, Social Security and, on the other, Medicare and other major health care programs, each of which account for about one-quarter of federal spending.

Taken together, these programs provide pensions or health insurance (or health insurance subsidies) to roughly half of all Americans. This total includes about 75 million elderly or disabled Americans, who account for some 85 percent of the spending on these programs (including about 95 percent of spending on Social Security and 75 percent of spending on major medical programs). In addition, it includes at least 40 million children and some 50 million low- to moderate-income adults (primarily beneficiaries of federal health insurance programs), who account for the remaining 15 percent of spending on these programs.

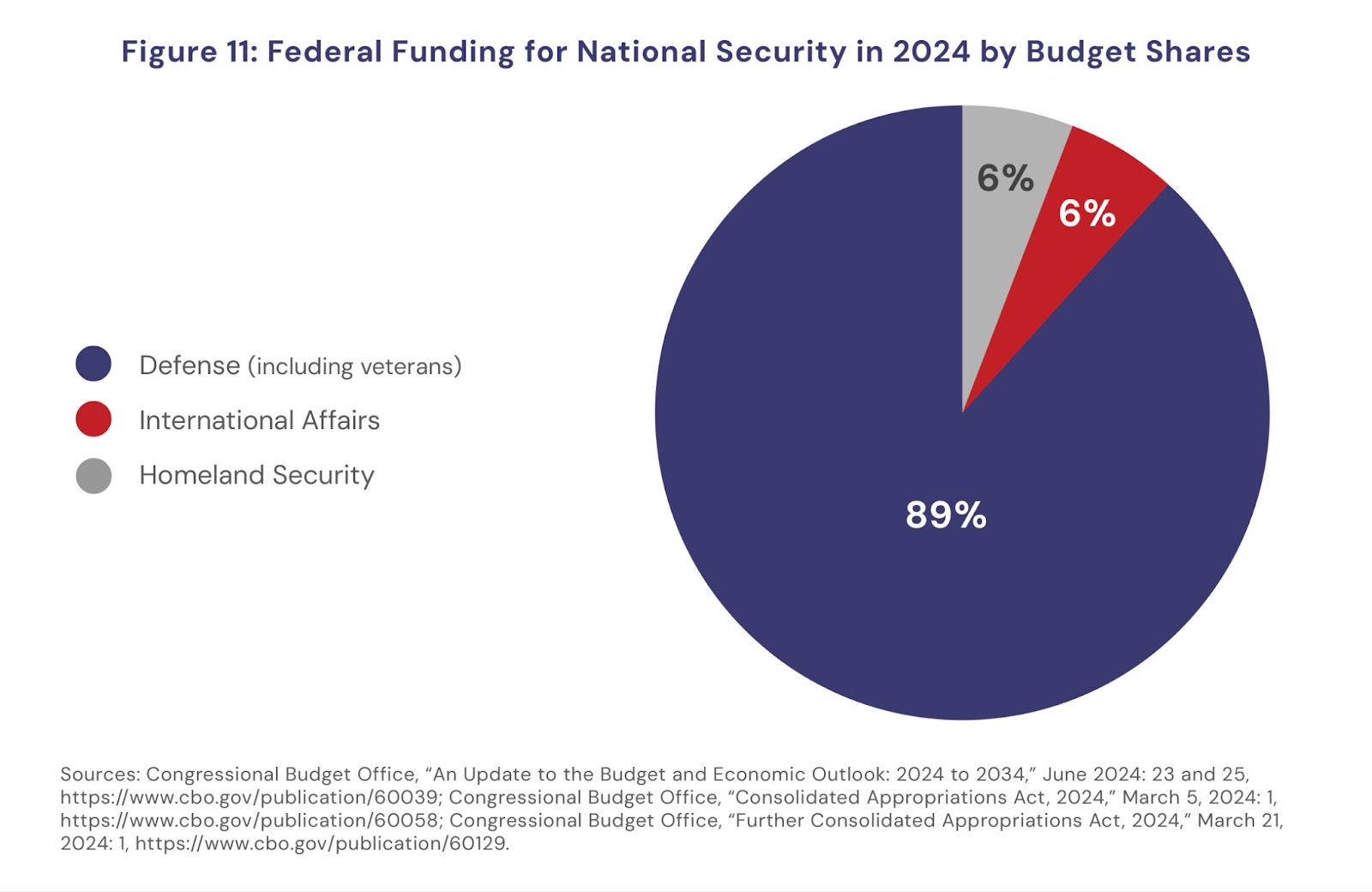

Another quarter of federal primary spending is allocated to national security. The vast majority of this spending — some 89 percent in 2024 — is used to support the U.S. military, including the Defense Department, other defense-related departments and agencies, and the Department of Veterans Affairs. The remaining 11 percent is roughly equally divided between international affairs spending and the Department of Homeland Security.

The last quarter of federal primary spending goes toward funding essentially everything else. In contrast to the other buckets noted above, this one consists of a very broad range of generally much smaller programs. Taken as a whole, the programs in this bucket have also been among the slowest-growing programs and are projected to continue to grow at a significantly slower rate than other areas of the federal budget. Perhaps oddly, given the smaller size of these programs and their slower growth, these are among the programs many Americans most associate with federal spending. They include, for example, federal spending on transportation, education, medical and other research, student loans, national parks, federal civilian civil service retirement benefits (non–Defense Department and Department of Veterans Affairs), agriculture price supports, housing assistance, the civilian space program, environmental protection, federal law enforcement, and public health programs.

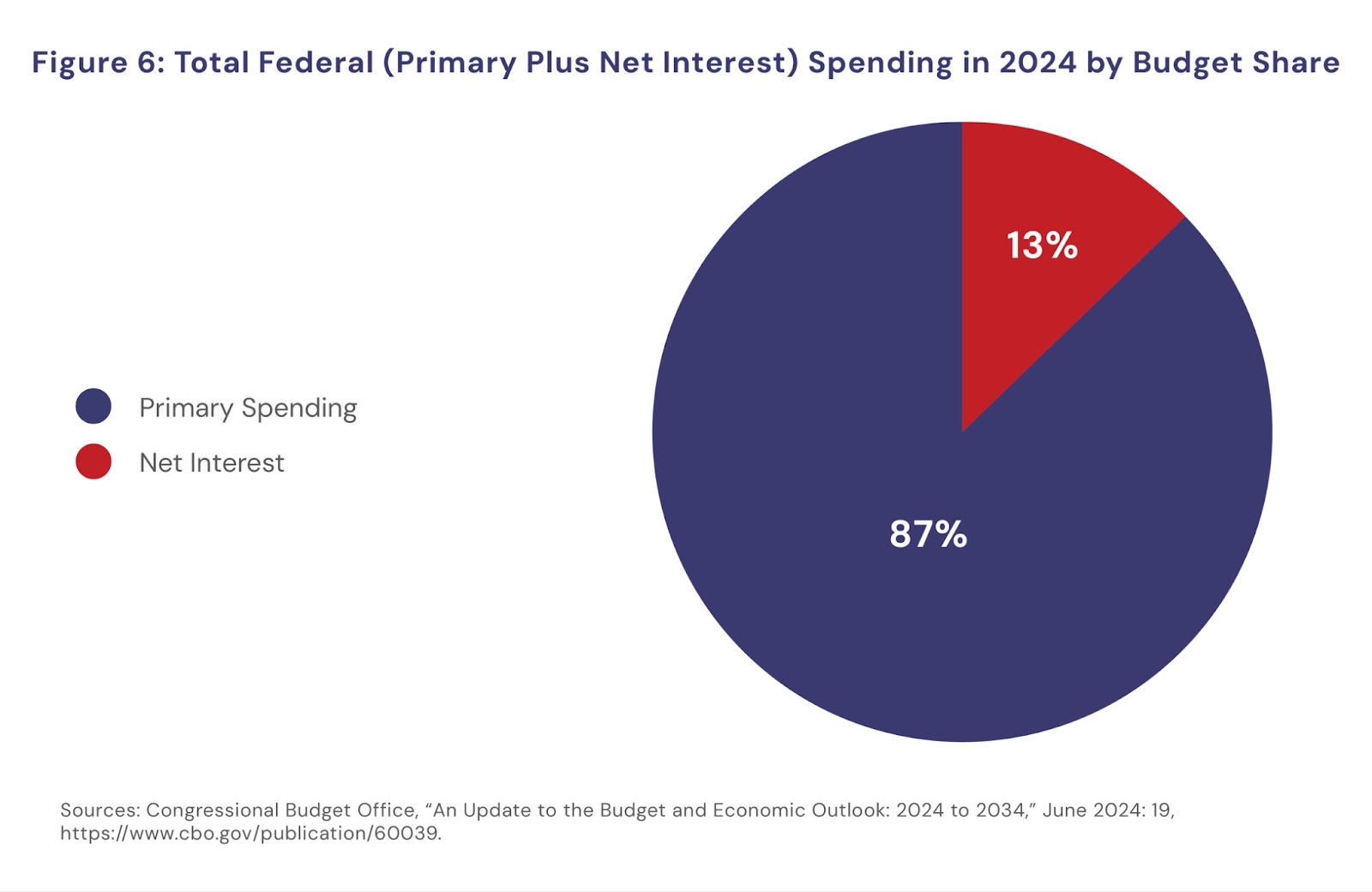

In addition to these three main buckets of primary spending, the federal budget also includes spending to cover the interest costs of servicing the debt. In 2024, net interest payments are estimated to account for about 13 percent of federal spending.16(See Figure 6.) Net interest is now the fastest-growing part of the federal budget. Although interest payments represent real spending no less than primary spending, conceptually it is useful to separate the two types of spending because they are driven by two very different mechanisms. Primary spending reflects the level of resources the country chooses to allocate to programmatic purposes, while spending on interest is largely a byproduct of the mismatch between spending and revenues.

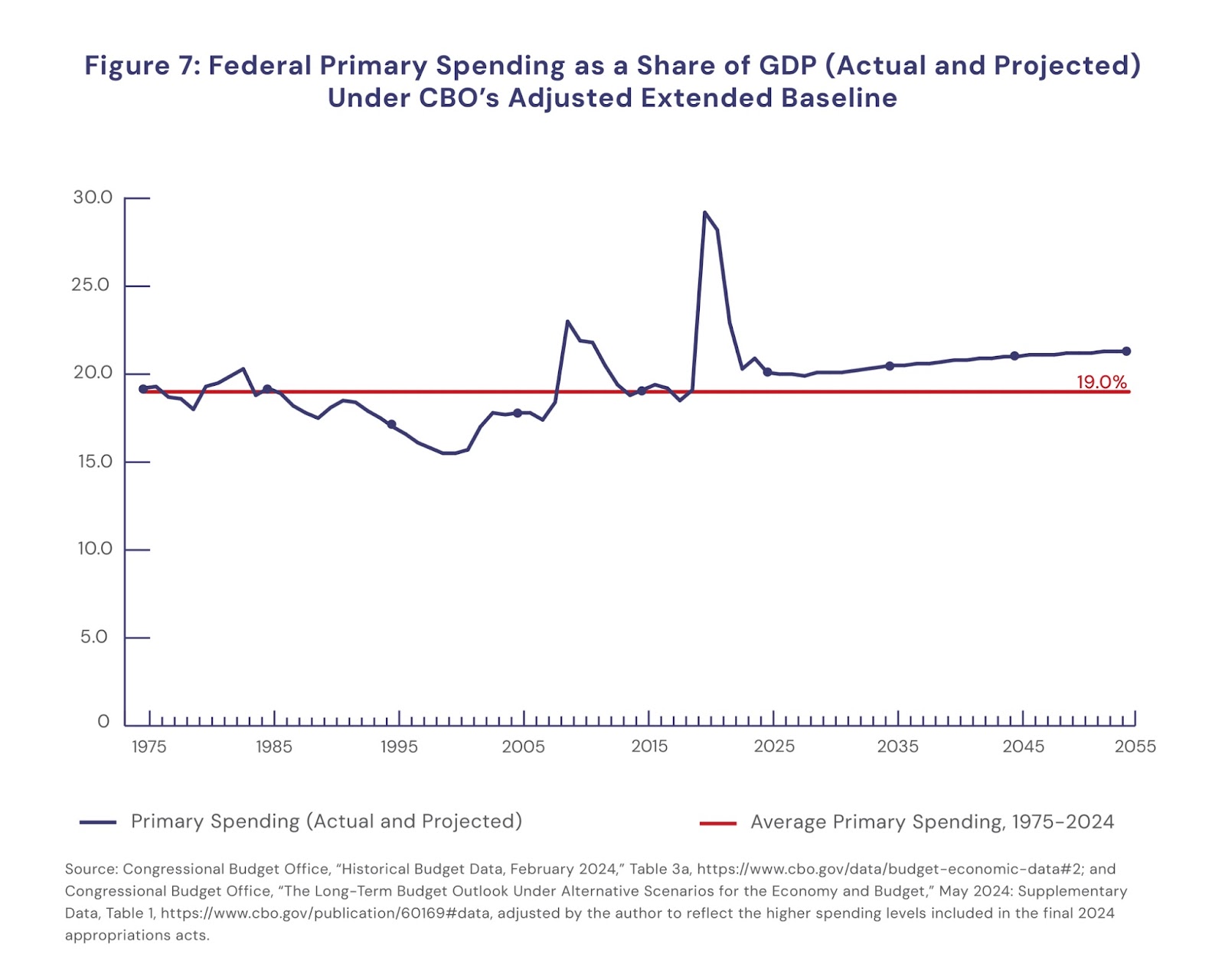

Understanding this distinction captures a critical reality that is otherwise generally missed entirely. The growth in the federal debt, both historically and as projected in coming years, does not stem from a major increase in the share of GDP allocated to federal spending on programs — that is, primary spending. To be sure, the composition of federal spending has changed considerably over time and is projected to continue to do so. But, measured by its share of GDP, federal primary spending has grown only relatively modestly over the past three decades and is projected to grow only relatively modestly over the next three decades. (See Figure 7.) In 2024, primary federal spending accounted for about 20.1 percent of GDP. This is less than one percentage point higher than the 19.2 percent share of GDP that primary spending absorbed on average over the past 30 years. Likewise, under CBO’s extended baseline scenario — which assumes the continuation of current laws and policies — adjusted to take into account the higher level of discretionary spending included in the final 2024 budget deal, primary federal spending would be projected to average about 20.7 percent of GDP over the next 30 years, just 0.6 percentage points above the 2024 share.17Even in 2054, federal primary spending is projected to absorb only 21.3 percent of GDP,18just 1.1 percentage points above today’s level.19

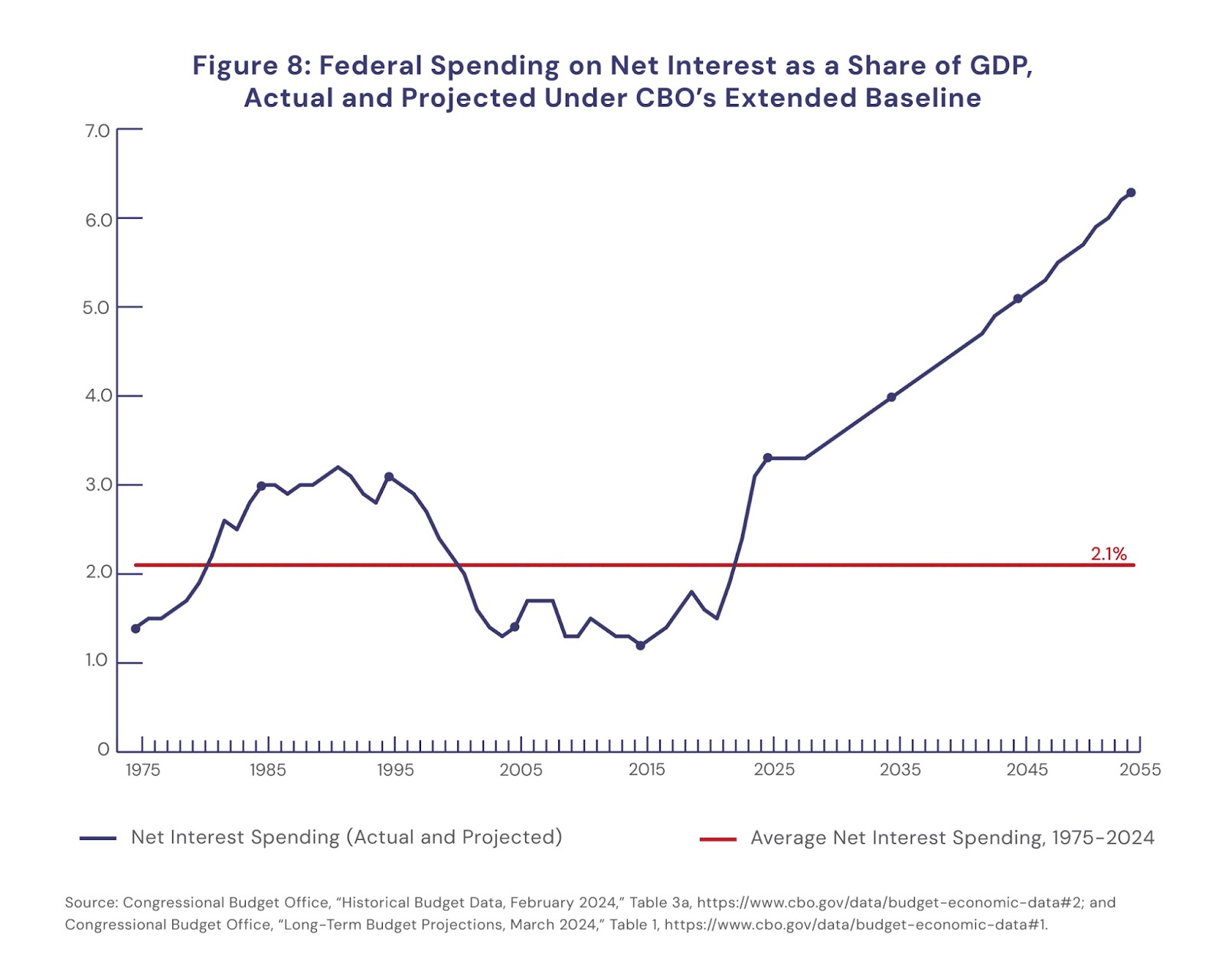

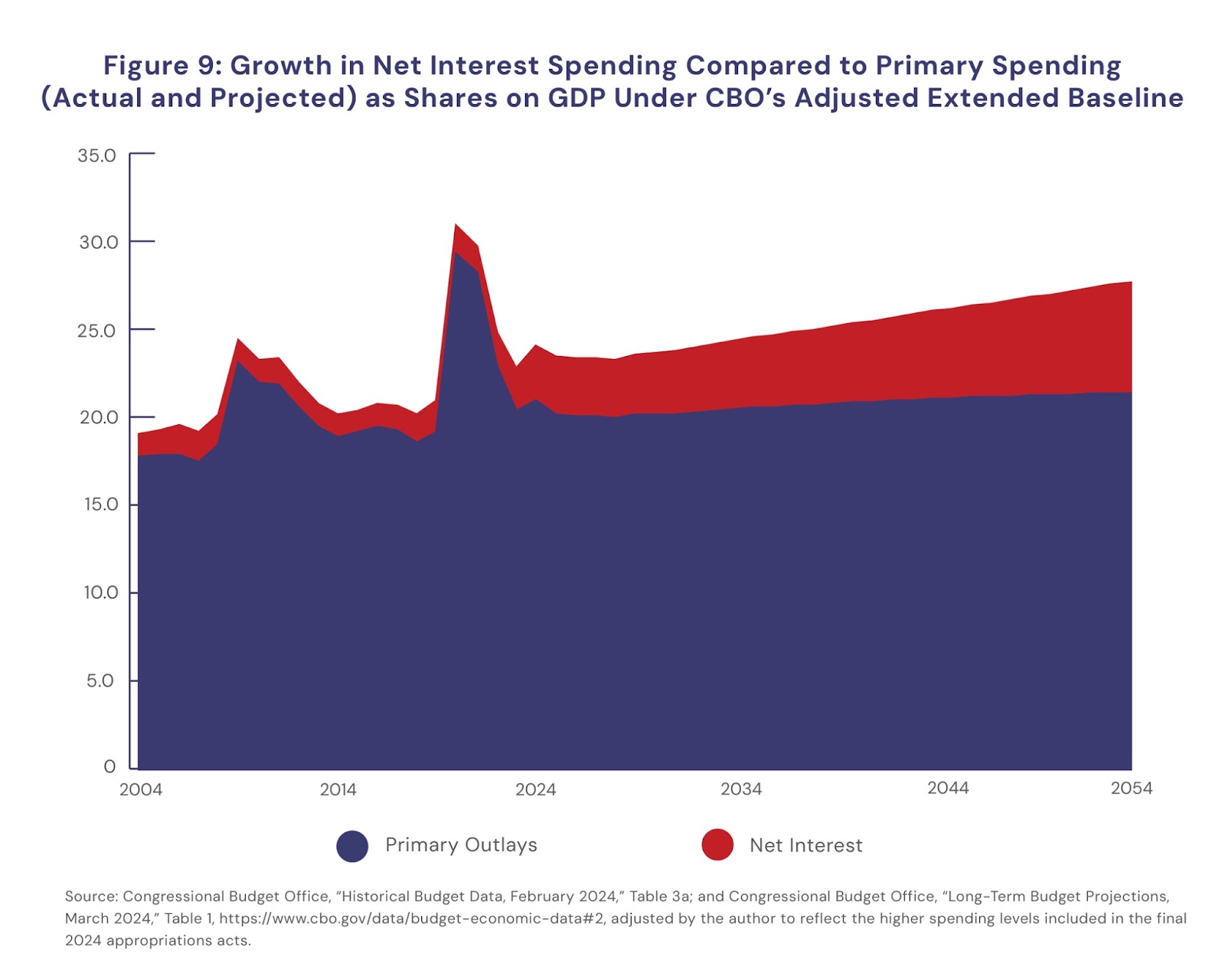

The real fiscal challenge facing the country today stems far less from projected increases in primary spending than the projected growth in spending on interest payments. Under CBO’s extended baseline scenario, spending on net interest is projected to grow from about 3.1 percent of GDP in 2024 to 6.3 percent of GDP in 2054. (See Figure 8.)

That growth is estimated to account for the vast majority of the increase in total spending (primary plus net interest) as a share of GDP projected by CBO in its extended baseline.20(See Figure 9.) The increase is driven by a combination of a growing mismatch between projected primary spending and revenue, and the impact of higher interest rates. As noted earlier, this interest-driven growth in the debt can be averted through relatively modest adjustments — in primary spending, revenue, or a combination of the two — that would close the fiscal gap.

A closer examination of the three different buckets of federal primary spending noted above makes it all too apparent why generating major savings in areas of federal spending outside of defense to fund a major increase in the defense budget would be so difficult and unlikely to materialize. Again, this is not to say that no savings in the nondefense portion of the federal budget can be found, only that the idea that large-scale savings of the magnitude needed to offset a massive, sustained increase in the defense budget — especially if combined with tax cuts — are extremely unrealistic. In the following section, this paper examines each of the three buckets of federal spending noted above in more detail — and the difficulties of making deep cuts in any of them.

The Three Buckets of Federal Spending

Federal spending on Social Security and other major health care programs

In this analysis, Social Security and Medicare and other major health care programs are considered as a single bucket of federal spending. (See Figure 10.) Although they could be thought of as two separate buckets of roughly equal size, considering them as a single programmatic area makes sense because both buckets of spending are largely focused on the same population: roughly 75 million elderly or disabled Americans.21As noted earlier, this population accounts for about 85 percent of the spending on these programs, including about 95 percent of spending on Social Security and 75 percent of the spending on Medicare and other major health care programs22— with elderly beneficiaries outnumbering disabled beneficiaries by a ratio of 7 or 8 to 1.23

Because elderly or disabled Americans account for the vast majority of spending in this bucket, they are the primary focus of the discussion below. But it is important to remember that at least 40 million children and some 50 million low- to moderate-income adults are also highly dependent on these programs — primarily for health insurance provided through Medicaid, the Children’s Health Insurance Program, and Affordable Care Act subsidies, but also for Social Security survivor and dependent benefits.24

This represents roughly 22 percent of America’s overall population if only the elderly or disabled are included, and nearly half the population if other beneficiaries are also included. On some level, the notion that cutting pension and health insurance benefits for them would be difficult is unlikely to come as a surprise to most readers with even the most casual understanding of these programs. However, going beyond such a casual understanding makes it far clearer just how difficult making such cuts would be to implement and why these programs are hugely popular with all Americans, not just beneficiaries.25Among the key reasons are these:

Beneficiaries are highly dependent on these programs, and that dependence is likely to grow. Roughly half of elderly Americans depend on Social Security for half or more of their income,26and one in four beneficiaries depend on it for 90 percent or more of their income.27Without Social Security, some 39 percent of elderly Americans would fall below the poverty line. Nor is the importance of Social Security limited to those of low or moderate means. Social Security benefits account for between one-quarter and one-third of the income even of many high-income retired Americans.28Likewise, average annual medical care costs for elderly Americans now rival the size of the average annual Social Security payment, making this population’s dependence on Medicare and other major health care programs equally great.29

Moreover, the importance of Social Security, Medicare, and other major health care programs is likely to increase further in coming years. The number of workers covered by private “defined benefit” pension plans has declined dramatically over the past several decades.30And, in part due to the relatively modest growth that has occurred in wages for the typical American worker over these years, contributions to 401(k)s and other defined contribution plans have fallen way short of what would be needed to provide anything like a comparable contribution to most Americans’ retirement income.31Similarly, the continued growth in health care costs means that the dependence of elderly or disabled Americans on Medicare and other major medical programs is likely to increase even more significantly.

While critical, these benefits are relatively modest. Even though America’s elderly or disabled are highly dependent on the Social Security and Medicare programs, the benefits provided by those programs are not overly generous. In 2023, the median Social Security benefit amounted to about $21,000 a year.32The level of working-age income replaced by Social Security is also well below that of comparable programs in most other developed countries. On average, Social Security replaces just 37 percent of the average person’s paycheck of their working years — leading many beneficiaries to suffer a steep decline in monthly income upon retirement. By comparison, on average, the pension systems of developed European and Asian countries replace 52 percent of the retiree’s working-age income.33Similarly, Social Security’s retirement age is higher than is common among most other developed countries.34It is also important to remember that, in the case of Medicare, beneficiaries must still pay substantial out-of-pocket medical expenses (e.g., for Medicare premiums, supplemental insurance, and services not covered by Medicare), which average some $5,000 annually — a significant burden given the limited income of most beneficiaries.35Not surprisingly, the relatively modest nature of the benefits provided — given the level of need — makes it difficult to contemplate significant reductions to these programs.

Beneficiaries contributed to the programs. The fact that Social Security and Medicare beneficiaries contributed extensively to the programs — through payroll tax contributions throughout their working years — also adds to the difficulty of contemplating reductions. Payroll taxes on workers’ wages allocated to Social Security and Medicare average 12.6 percent and 2.9 percent, respectively.36Having paid into these programs throughout their working lives (and, in the case of Medicare, continuing to contribute through the payment of substantial premiums), beneficiaries view the benefits as a right, not a privilege — understandably so.

Social Security, Medicare, and other major health care programs are highly efficient. Another factor that works against major cuts to Social Security and major federal health care programs is that they are — in terms of administrative expenses and, in the case of health care programs, cost controls — relatively efficient compared to their private sector counterparts. Administrative expenses account for only 0.5 percent of Social Security’s annual benefits, far below the percentages for private annuities.37Medicare’s administrative expenses are likewise lower than those of private health insurance plans. Moreover, on a per capita basis, over the past 30 years Medicare spending has grown more slowly than has spending on those covered by private health insurance plans.38

The number of Americans who would be hurt by cuts to these programs far exceeds the number of current, direct beneficiaries. As high as the number of direct beneficiaries of Social Security and major health care programs is, that total greatly understates the number — and age range — of Americans who would be negatively affected by cuts to these programs.

Most obviously, this is because virtually all Americans, unless they die prematurely, will become Social Security and Medicare beneficiaries. In other words, while at any given time only a fraction of Americans receive these benefits, over the course of their lifetimes, virtually all Americans will become beneficiaries — including the 184 million workers now in jobs that pay into Social Security.39It is worth noting as well that this characteristic of the Social Security and Medicare programs is hardly unique to these programs. At the other end of the age spectrum, public education, at least through high school, is another age-specific government program from which virtually all Americans benefit over the course of their lifetimes. This is even though at any given time, only a fraction of Americans are enrolled in the country’s primary and secondary schools, as well as public colleges and other institutions of postsecondary education and training.

However, for tens of millions of Americans still in their working years, cuts to Social Security and Medicare would pose a particularly immediate and severe challenge. This includes those Americans nearing retirement age, who would have too little time to significantly reduce their dependence on these programs by, for example, lowering their current spending to increase their personal retirement savings. Even if we define this category relatively narrowly to include only those 54 to 64 years of age, this adds some 40 million Americans to those with a clear, near-term dependence on these benefits.

But even this greatly understates the number and age range of Americans who would face significant and immediate negative consequences to cuts in Social Security and Medicare. To the groups of Americans currently receiving these benefits and those nearing retirement age, add those working-age Americans who have elderly parents. The vast majority of the 83 million working-age Americans in their 40s and 50s have at least one elderly parent. Even with the income provided by Social Security and the health insurance provided by Medicare and other major medical programs, roughly one in five of those working-age adults typically provide some amount of financial support to their parents.40

If Social Security and Medicare and other major medical programs were cut significantly, that share of the working-age population would have to provide such support given the very broad (and understandable) view that adult children have a responsibility to elderly parents in need.41This would be especially difficult for the more than half of working-age adults in their 40s and 50s who both have at least one elderly parent and currently provide financial assistance to minor or adult children. Unsurprisingly, one study found that such “sandwich generation” working-age adults who needed to provide financial support for their parents were notably less likely to describe their household financial situation as “living comfortably” and significantly more likely to describe it as “just meeting basic expenses” than those who did not need to provide such financial assistance.42With cuts to Social Security and Medicare and other major medical programs, the financial situation of such households would deteriorate further. This would have serious financial implications not only for the working-age adults in those households but for the elderly parents dependent on them for support.

In summary, in considering the negative impacts of cutting Social Security, Medicare, and other major health care programs, it is not enough to consider only the effect on current, direct beneficiaries. One needs to add those who are nearing retirement age, those working-age adults who would need to step in to provide financial support (or greater financial support) to their elderly parents, as well as the minor and adult children of those parents who would likely see some offsetting reduction in support. And when those groups are added, the proportion of the American population with a stake in these programs in a very meaningful, immediate, and tangible sense grows beyond the 22 percent of the U.S. population accounted for by elderly or disabled direct beneficiaries — or even the roughly half of the U.S. population accounted for when children and working-age beneficiaries are included — to a substantial majority of Americans, across all age ranges. The intergenerational character of those directly and indirectly benefiting from these programs, and the degree to which beneficiaries have contributed to the financing of these programs over their lifetimes, also illustrates how unhelpful and misleading it is to portray these programs as somehow representing simple transfers of wealth to the elderly from working-age and younger Americans.43

The discussion above also underscores what should be an obvious point, but one that often seems to get lost: Proposals to cut spending on Social Security, Medicare, and other major health care programs are generally much less about reducing costs than about shifting costs. Policy changes that promise to yield savings in terms of the share of GDP accounted for by these government programs in future years are — not surprisingly — likely to be opposed by the large segment of the U.S. population that is dependent on these programs, especially if the “savings” are achieved by merely shifting those costs from the government to individuals and families.44

Federal spending on other nonsecurity programs

Unlike the other two major buckets of federal spending discussed here, which are both focused on relatively clearly defined programmatic areas, other nonsecurity spending includes a broad range of programs. That said, for purposes of discussion, it is useful to divide these programs into three subcategories. Doing so helps further clarify why, here too, making major reductions in spending to offset proposed increases in defense spending would be difficult both politically and practically. The three subcategories, each accounting for roughly one-third of other nonsecurity spending, consist of investment, income security, and other federal programs.

Investment programs: Federal investment spending consists of spending focused on goods, services, and other activities that are expected to contribute to the country’s economic growth in future years. There is considerable debate over how much federal spending, and which particular programs, effectively contribute to such growth. Here, a relatively narrow definition of investment programs is used, consistent with the methodology developed by the Congressional Budget Office, CBO.45This definition focuses primarily on spending on physical infrastructure (e.g., roads and bridges), education and training, and research and development. Based on CBO’s analysis of 2018 data, a reasonable estimate is that in 2024, federal nonsecurity spending on these types of programs amounted to about $430 billion, equivalent to 31 percent of other nonsecurity spending.46

This area of federal spending would seem like an especially odd place to consider deep reductions to pay for an increase in defense spending. This is because China’s spending in similar areas of investment is widely considered a key underpinning of the meteoric growth of its economy over the past several decades. That growth, in turn, has largely underwritten its growth as a major military power. Indeed, some analysts who have expressed concern about China’s rise as both an economic and military competitor of the United States have lamented that U.S. spending on such programs — which has generally declined as a share of the economy over the past two decades47— has not significantly increased.

Income security: This category consists of programs focused on providing support for low-income individuals, primarily children, families with children, the elderly, and the disabled. With a combined budget of about $490 billion in 2024, these programs account for some 35 percent of other nonsecurity spending. The specific programs include:48

- Supplemental Nutrition Assistance Program, SNAP ($105 billion). SNAP provides modest food assistance (averaging $189 per month in 2024) to very low-income Americans (92 percent of the benefits go to those below the poverty line), the vast majority of whom either work in low-paying jobs or are unable to work. About two-thirds of recipients are families with children and one-third include at least one elderly or disabled adult.49

- Rental assistance ($66 billion): Federal rental assistance programs help low-income Americans cover the cost of housing in cases where the rent typically exceeds half of their income. Here, too, the vast majority (over two-thirds) of recipients are in households that include children, or an elderly or disabled adult.50

- Supplemental Security Income ($62 billion): This program provides modest payments (averaging $943 a month) to very poor elderly or disabled individuals, most of whom have no other source of income, and the vast majority of whom (84 percent) are severely disabled.51

- Child nutrition, family support, and foster care ($78 billion): These programs provide support for, respectively, subsidized school lunches and breakfasts for children of low-income families, and foster care and related activities.

In addition to these specific program areas, this subcategory includes some $190 billion in funding for a range of other programs. Many of these other programs are also focused on children of low-income families, including Head Start, other child care and preschool programs, and the Child Tax Credit. This total also includes funding for the Earned Income Tax Credit, unemployment insurance, and a number of other programs.

Given the extremely vulnerable nature of the populations served by these programs — generally very low-income individuals and households, and largely focused on children, the elderly, and the disabled — proposals to cut funding to these programs are also, understandably, likely to generate strong resistance.

Other federal programs: This subcategory includes all other federal programs not covered elsewhere in this paper. In 2024, spending on this wide range of programs totaled some $480 billion, accounting for 35 percent of other nonsecurity spending. Unlike the case with the other two subcategories of funding described in this section, there is no broad descriptive term that can be used to meaningfully describe the purpose of these programs — there is just too much diversity among these programs and activities. Nothing in the diversity of the agencies and programs funded through this subcategory, however, suggests it would be any easier to cut funding for these programs. Indeed, among them are many that a large number of Americans would likely see as critical and representing core government functions. They include funding for:

- Law enforcement, the federal court system, and other Justice Department activities ($81 billion).

- The Centers for Disease Control and Prevention, perhaps the key agency focused on pandemic surveillance and response ($9 billion).

- Administrative costs associated with the Social Security and Medicare programs ($15 million).

- Natural resources and environment programs, including the Forest Service, National Park Service, National Oceanic and Atmospheric Administration, Environmental Protection Agency, and the U.S. Fish and Wildlife Service ($81 billion).

Federal spending on security programs

The third main bucket of primary federal spending consists of spending on national security. The departments and agencies included in this category of analysis are the same as those used in the definition agreed to by the Obama administration and Congress for the first year of the Budget Control Act, BCA, of 2011, when the discretionary budget caps were divided between security and nonsecurity programs (for later years of the 10-year BCA, the caps switched to defense and nondefense). They include the Department of Defense and other, smaller defense-related agencies, such as the National Nuclear Security Administration (part of the Department of Energy), that fall under the official “National Defense” line of the federal budget, as well as the Department of Veterans Affairs, the international affairs budget, and funding for the Department of Homeland Security.

As noted earlier, the vast majority of the funding for these programs is used to support the U.S. military, including active and reserve military forces, and military retirees and veterans. Taken together, today these programs account for about 89 percent of the spending in the national security bucket. (See Figure 11.) The remainder of the funding in this bucket is split relatively equally between spending on international affairs and homeland security. In theory, some portion of nondefense security spending could be cut to help offset an increase in defense spending. As a practical matter, however, it is very difficult to see how it would prove feasible — even if such a shift in spending seemed appropriate from an overall U.S. national security standpoint.

Funding for homeland security enjoys broad support and represents a critical component of our national security. Moreover, few advocates of increasing defense spending appear to contemplate, let alone advocate, cutting funding for homeland security as a means of paying for such an increase. Likewise, the international affairs budget is widely seen — including among the country’s senior military leadership — as critical to supporting the nation’s national security strategy. In part this reflects a view that foreign aid — in areas like humanitarian assistance, development assistance, and global health — plays an important part in raising America’s stature and “winning hearts and minds.” But it also reflects an understanding that much of the U.S. international affairs budget is focused on directly supporting U.S. national security interests through economic and security assistance. This assistance is often focused on key U.S. strategic partners, including in areas of active military conflict, such as Ukraine today and, in the recent past, Afghanistan and Iraq.52In any event, in budgetary terms, both the homeland security and international affairs budgets represent relatively small pots to draw from.

What makes it especially implausible that a major increase in defense spending might be offset through cuts in other national security programs — even modestly and partially — is that by far the largest of these other areas, veterans’ benefits, is almost certainly off the table as a source of funding to draw from. Veterans’ benefits account for some 22 percent of U.S. national security spending. As noted earlier, these programs have not only proven extremely resistant to cuts, but have enjoyed major, sustained increases in funding. The history of the past two decades suggests that, even if it were somehow deemed possible and wise to trim spending on homeland security or international affairs to help pay for a major increase in defense spending, any such offset would be greatly overshadowed, and overwhelmed, by pressures to grow the share of security spending allocated to veterans’ benefits.

Trends in federal spending

Another important consideration in the difficulty of making major reductions in nondefense programs and spending is the different trends associated with different parts of that spending. Most notable is that the two largest and most popular nondefense programs — Social Security and Medicare — are also the two nondefense programs with the greatest projected growth. Indeed, under CBO’s extended baseline, Social Security and major health care programs account for all of the projected growth in federal primary spending as a share of GDP. Other primary spending is actually projected to decline significantly as a share of GDP, offsetting much of the growth projected for Social Security and Medicare. This variable growth rate is why overall primary spending is projected to increase only relatively modestly as a share of GDP over the next three decades.

Specifically, under CBO’s extended baseline, spending on Social Security and major health care programs is projected to grow by a total of 3.3 percent of GDP between 2023 and 2054 — with the vast majority of that growth (2.5 percent of GDP) associated with major health care programs, Medicare in particular. Essentially all of the growth projected for Social Security spending (equivalent to 0.8 percent of GDP) is driven by the growth in the elderly’s share of the U.S. population, which is projected to increase from 18 percent in 2023 to 22 percent by 2054.53However, such growth accounts for only about one-third of the growth in spending projected for Medicare and other major health care programs. Two-thirds of the growth is accounted for by projected increases in per capita health care spending, which CBO projects will — as in the past — increase significantly above the rate of growth projected both for overall inflation and the economy.54

Conversely, in its extended baseline, CBO projects that all other primary federal spending combined will decline by about 2.6 percent of GDP.55A little over half of this decline is based on the assumption that the share of primary spending allocated to discretionary programs will continue to decline as a share of GDP, as it has over the past several decades.56Slightly under half of this decline is projected to result from the fact that — unlike the case with health care spending — spending per capita on benefits for most other mandatory programs is projected to grow consistent with the overall inflation rate, and more slowly than the rate of growth projected for the economy.57Taken together, the projected increases in Social Security and Medicare spending as a share of GDP and the projected declines in other primary spending as a share of GDP yield a total increase in primary spending that is projected to reach about 1.1 percent of GDP by 2054.

Managing the Federal Debt

Absent any realistic prospect that the massive increase in defense spending advocated by some today would be paid for through deep cuts in other spending, the proposed buildup would dramatically exacerbate the problem posed by the federal debt. Among other things, it would more than double the difficulty of stabilizing that burden in coming years. If, moreover, such a buildup in the defense budget were to be combined with a large tax cut, the repercussions would be worse still.

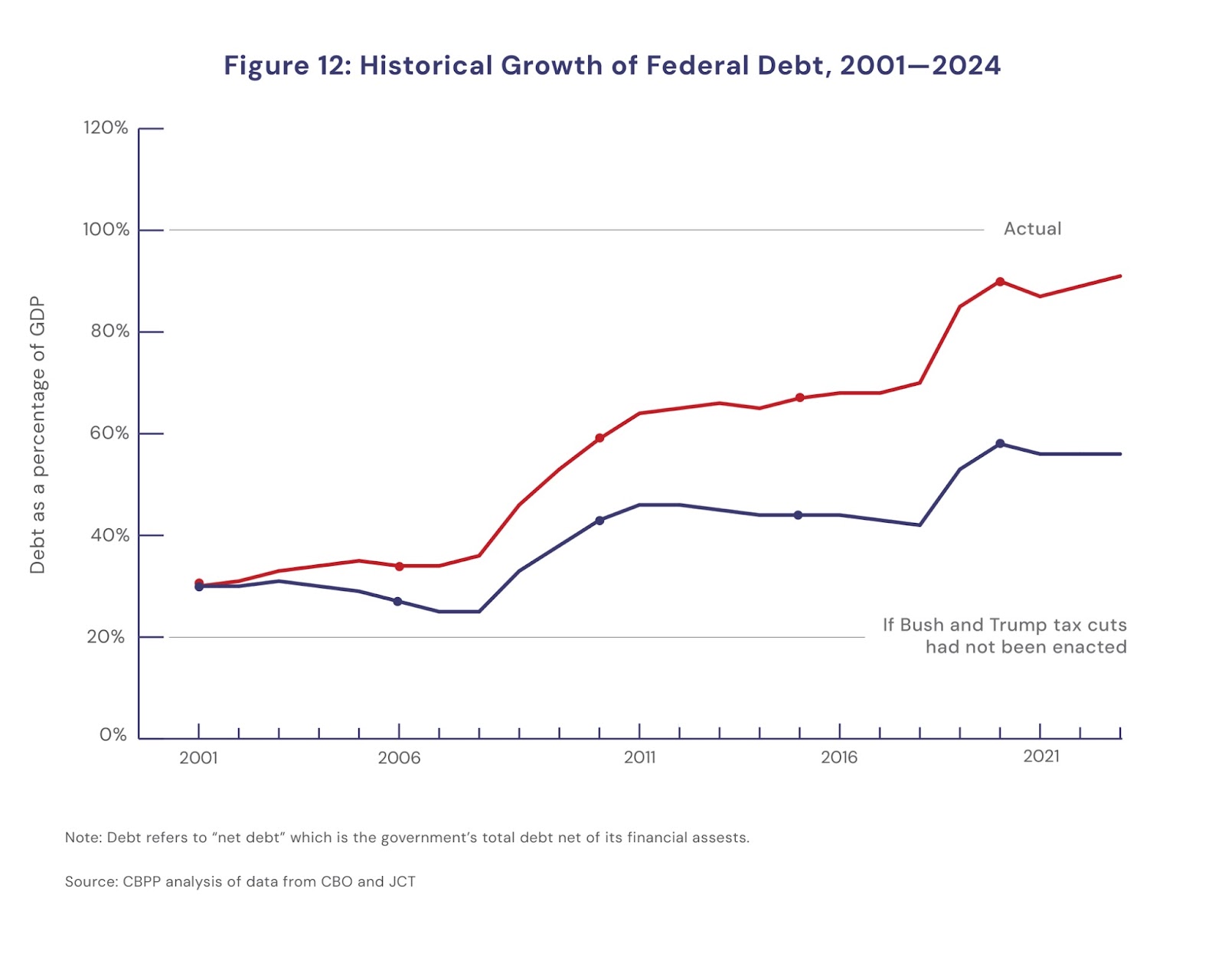

The federal debt has increased substantially over the past several decades, fueled largely by increased spending and lower revenue associated with the Great Recession and the COVID–19 pandemic, and the large George W. Bush administration and Trump administration tax cuts. (See Figure 12.) As a result of these factors, the size of the publicly held federal debt grew from the equivalent of about 30 percent of GDP in 2000 to an estimated 99 percent of GDP in 2024.58According to CBO’s most recent long-term budget analysis, (i.e., CBO’s extended baseline scenario), the debt is projected to increase to some 166 percent of GDP by 2054.59Moreover, this estimate was originally published prior to enactment of the final 2024 budget deal, which included additional funding not assumed in CBO’s baseline scenario — suggesting that this projection at least modestly understates the likely size of the debt in 2054.

Notwithstanding this mushrooming of the debt over the past several decades and the significant additional growth projected under current policies, if policymakers were to make relatively modest changes in those policies — at least in mathematical terms — the projected growth of the federal debt could be averted. CBO’s most recent analysis of the long-term budget outlook — projecting the debt will reach 166 percent of GDP in 2054 — implies a fiscal gap of about 1.3 percent of GDP. 60

In other words, based on CBO’s most recently published long-term budget analysis, the federal debt could be stabilized at today’s share of GDP over the long term, if policymakers were to agree to implement (and sustain) some combination of cuts in primary spending and tax increases equivalent to about 1.3 percent of GDP. Adjusting CBO’s extended baseline estimate to take into account the higher discretionary spending level included in the final 2024 budget deal — reached after CBO’s analysis was released — suggests a slightly larger fiscal gap of about 1.5 percent of GDP.61Under CBO’s extended baseline scenario — again adjusted for the higher spending in the final budget deal — federal primary spending would average about 20.7 percent of GDP, while revenues would average 18.2 percent of GDP over the next 30 years.62Given a fiscal gap of 1.5 percent of GDP, this means that the debt-to-GDP ratio could be stabilized at today’s level if a budget deal permanently:

- Reduced primary spending from its currently projected average share of GDP of 20.7 percent to 19.2 percent, which would essentially require a 7 percent reduction in the share of GDP allocated to primary spending, or

- Increased taxes from their currently projected average share of GDP of 18.2 percent to 19.7 percent, which would essentially require an 8 percent increase in the share of GDP allocated to federal taxes, or

- Both reduced primary spending and increased taxes, which — if allocated equally between the two — would require only roughly a 4 percent decrease in the share of GDP allocated to primary spending and a 4 percent increase in the share allocated to federal taxes.63

Stabilizing the debt would be a huge step in addressing the country’s long-term fiscal health. As the term implies, it would mean that the debt would stop growing as a share of the economy. As such, it would be sustainable over the long run. Moreover, a stable debt-to-GDP ratio would improve the country’s projected economic growth rate.

The relative ease — at least in terms of the math of the required budgetary adjustments — with which the debt-to-GDP ratio could be stabilized shows the power relatively small policy changes can make when they are compounded over a significant period of time. Under CBO’s extended baseline projection, the federal government will run “primary deficits” (annual primary spending minus annual revenue) averaging about 2.2 percent of GDP, plus net interest costs averaging 4.5 percent of GDP, for overall deficits averaging 6.8 percent of GDP.64As a result, in its extended baseline, CBO projects that between 2024 and 2054, the size of the publicly held debt will grow from about 99 percent to 166 percent of GDP.65

However, CBO also provides an alternative scenario in which the debt-to-GDP ratio stabilizes at 99 percent of GDP. Such an outcome could be achieved if — as noted above — policymakers were to agree to implement (and sustain) some combination of cuts in primary spending and tax increases equivalent to about 1.5 percent of GDP.66Doing so would reduce overall deficits by 3.1 percent of GDP — compared to CBO’s extended baseline scenario — to an average of 3.6 percent of GDP over the 30 years and would stabilize the debt at a 99 percent share of GDP. The reason a larger reduction in primary spending or increase in taxes would not be needed to achieve this reduction in overall annual deficits of 3.1 percent of GDP is that the change in policy would also affect net interest costs and economic growth — yielding additional savings.67According to CBO, about two-thirds of these additional savings would result from lower interest costs and one-third from higher economic growth (which would have the effect of both increasing revenues and lowering the share of GDP accounted for by a given level of spending).68

In sum, based on data and analysis provided by CBO, implementing and sustaining a combination of spending cuts and tax increases equivalent to just 1.5 percent of GDP would be projected to cause overall deficits to drop from an average of 6.8 percent of GDP over the long run to an average of 3.6 percent of GDP — when the knockoff effects on interest costs and growth of the economy are factored in.69In turn, with average overall deficits of that size, the debt-to-GDP ratio would be projected to stabilize at today’s level.

As the above discussion shows, if the political will can be generated, stabilizing the federal debt burden is well within the county’s means. There is nothing inevitable about the growth in the debt projected under current law and policies. As noted earlier, the risk of a mushrooming debt burden is not the result of out-of-control increases in spending on federal programs. As a share of GDP, federal primary outlays over the next 30 years, under CBO’s adjusted extended baseline scenario, would be projected to average 20.7 percent of GDP, compared to the 19.2 percent average of the past 30 years.70Rather, the risk stems from the dramatic growth projected for spending on net interest, which under the CBO extended baseline scenario is projected to increase from 3.1 percent of GDP today to an average of 4.5 percent of GDP over the next 30 years, and reach 6.3 percent of GDP by 2054.71That growth — as shown in CBO’s alternative scenario — can be effectively addressed with relatively modest policy changes to primary spending and revenue.

Unfortunately, the compounding effect of small policy changes can also work in the opposite direction — to dramatically exacerbate, rather than reduce, the debt burden. Increasing the share of GDP allocated to defense from some 3.2 percent today to 5.0 percent by 2030 (and an average of 4.9 percent across the next 30 years) — up from about an average of about 2.7 percent under CBO’s adjusted baseline projections — without making offsetting cuts elsewhere in the budget, would increase the fiscal gap by 2.2 percent of GDP.72It would also cause a dramatic expansion of the debt burden. (See Figure 13.) In this case, the same knockoff effects noted for their positive impact in CBO’s alternative stable debt-to-GDP ratio scenario, would work in the opposite direction. Spending on net interest would increase from currently projected levels and the economy would grow more slowly, yielding lower revenues and increasing the share of GDP accounted for by a given level of spending. A reasonable estimate is that this policy change would increase the growth in the debt projected for 2054 from about 166 percent of GDP to some 260 percent of GDP.73

Worse yet would be a situation in which this major increase in defense spending was combined with a significant reduction in revenue, as has been the case with each of the past three major defense buildups since the 1980s. The most likely revenue reduction would involve extending the Trump administration tax cuts, which are otherwise set to expire in 2025. This would increase the size of the fiscal gap by about 1.2 percent of GDP.74Moreover, notwithstanding much rhetoric to the contrary, tax cuts clearly do not come close to paying for themselves — especially when they are financed through borrowing. Three different analyses, by a range of different economists and organizations, have estimated that extending the Trump administration tax cuts would have only an extremely modest impact on economic growth. As a result, they estimate that its extension would — through the feedback effect of higher economic growth on tax revenue — cover only 1 to 5 percent of the revenue loss directly attributable to the tax cut.75By itself, making the Trump administration tax cuts permanent would increase the debt-to-GDP ratio to some 210 percent of GDP by 2054.76

In combination, enacting both the proposed increase in defense spending and a permanent extension of the Trump administration tax cut would increase the fiscal gap by a total of about 3.4 percent of GDP (2.2 percent of GDP for the defense buildup plus 1.2 percent of GDP for extending the Trump administration tax cuts) compared to CBO’s extended baseline. Under these circumstances, a reasonable estimate is that the debt would grow to something close to 310 percent of GDP by 2054 — nearly double the level of debt projected for 2054 under CBO’s extended baseline scenario.77

Risks of a growing debt

The United States is a large and wealthy country, and it can carry a substantial level of debt and annual deficits without posing a significant risk to its financial stability or long-term economic growth. Countries such as Japan have significantly higher debt-to-GDP ratios than does the United States.78And there is no “magic number” past which all economists agree that the U.S. debt-to-GDP ratio becomes too high. As noted earlier, many economists believe that stabilizing the ratio of publicly held government debt to GDP at today’s level of 99 percent would suffice to ensure the sustainment of both of these goals. Even moving toward a much higher debt-to-GDP ratio of 200 percent or more might represent a sustainable debt burden for the United States — if it can be stabilized at that level.79

However, the growth of the federal debt described in this paper — driven by a massive unpaid-for increase in defense spending and tax cuts — would be well above these levels and on anything but a stable and, thus, sustainable course. As discussed earlier, under this set of policies, the level of publicly held federal debt would reach over 300 percent of GDP by 2054, and it would be on course to continue to grow at an even greater pace in the years beyond.

Among economists, the financial community, and policymakers, concerns about the rising debt-to-GDP ratio center on four main areas: the effect on long-term economic growth, the effect on the country’s ability to respond to significant economic downturns, the inefficiencies associated with excessive borrowing, and the potential for such borrowing to trigger a financial crisis. An acceleration of the debt along the lines outlined in this paper would dramatically exacerbate all of these dangers — with considerable potential impact on American national power.

Economic growth. One of the most frequently expressed concerns about a debt that grows faster than the economy is that federal borrowing may act to crowd out borrowing by the private sector, thereby inhibiting the long-term growth of the economy. The historically low real interest rates that have been common the past few decades suggest that this crowding out effect has been relatively modest in the recent past. It is inherently difficult to determine the effect of competition from federal borrowing on private sector growth. However, CBO and others project that, as federal borrowing grows, the effect could be very large. For example, CBO’s latest modeling of alternative long-term economic scenarios finds that the continued rapid growth in federal debt from current levels could reduce GDP in 2054 by as much as 10 percent, or approximately $8 trillion annually, as compared to what it could be if federal debt were stabilized at its current 99 percent share of the economy.80

Responding to economic downturns. Another concern is that, as the debt burden grows, it will become increasingly difficult for policymakers to respond effectively to economic downturns. Virtually all economists believe that during a recession it is appropriate — and often critical — for the federal government to run large deficits that grow the debt in order to help stimulate the economy and assist the unemployed and others affected by the downturn. Such countercyclical policies have been widely employed and supported by both Democratic and Republican administrations — even if the relative emphasis given to taxing and spending policies has differed between the two. It is easy to forget the importance of such policies when the economy is relatively strong, but historically such temporary, countercyclical measures have proven critical in getting the country through deep economic downturns — such as the Great Recession and the recession triggered by the COVID–19 pandemic, when unemployment reached 11 percent81and almost 15 percent,82respectively. As the size of the debt burden grows, the ability to respond with such measures is likely to be perceived as increasingly risky — especially as concerns about the dangers of a financial crisis linked to the federal debt similarly grows.

Cost of borrowing. A third concern associated with a growing debt-to-GDP ratio is the inefficiency of spending such a large share of the federal budget covering interest payments. In 2000, net interest accounted for about 12 percent of federal spending and 2.2 percent of GDP. By 2024, these shares had grown to 13 percent and 3.1 percent, respectively. Under CBO’s extended baseline scenario, these payments are projected to grow to much more significant levels over the next three decades — to some 23 percent and 6.3 percent, respectively, in 2054. And accelerating the growth in the debt burden through a massive increase in defense spending and additional tax cuts would cause a far more dramatic increase in spending on net interest payments. Under that scenario, net interest payments would balloon to 36 percent of federal spending and some 13 percent of GDP. At that point, federal spending on net interest would exceed federal spending on any other major area of the budget, including Social Security and Medicare combined, and would be more than two-and-a-half times greater than spending on defense. A related concern is that a significant share of interest payments would be paid to foreign investors (both governments and private sector investors), which at the end of 2023 held about 29 percent of the U.S. publicly held debt.83

Risk of financial crisis. Among the greatest concerns is that excessive federal borrowing that appeared to be on an unsustainable course could, at some point, trigger a financial crisis as bond holders lost faith in the capacity of the U.S. government to service its debt. Such a crisis would dramatically weaken the federal government’s capacity to borrow and would have severe economic repercussions. Among the consequences of such a financial crisis would be not only a dramatic drop in America’s prestige and standing — with likely significant implications for our competition with China — but a much more direct impact on the defense budget, as the federal government’s capacity for borrowing collapsed. Although a detailed analysis of how the defense budget would likely be affected by such a crisis is far beyond the scope of this paper, it is difficult to imagine a scenario in which the U.S. defense budget would escape a period of deep and sustained cuts. To be sure, as noted earlier, no one can predict with certainty when a large debt burden becomes too much debt and would trigger such a financial and economic calamity. But few doubt that the risk is real. And clearly the risk of such a financial crisis will grow dramatically should the debt burden grow along the lines described in this paper — specifically, on a course that not only leads to an unprecedentedly high U.S. debt burden, but shows no signs of stabilizing.

Individually, each of these four concerns described above provides a clear warning about the risks associated with the kind of unrestrained deficit spending that would realistically be the inevitable result of implementing a massive new defense buildup, especially if combined with further tax cuts. Taken together, they provide a compelling argument that pursuing such a policy path would be extremely reckless.

Conclusion

The case for a massive increase in defense spending — specifically, for increasing defense spending to 5 percent of GDP — is anything but compelling. There is no need, on national security grounds, for defense spending this large. The United States already spends far more on defense than does China, and enjoys an advantage in defense spending in excess of what it did over the Soviet Union during the Cold War.

Those who nonetheless believe that a massive increase in defense spending is needed should at least have the courage and realism to acknowledge that a significant tax increase would be needed to help pay for such a buildup. However, many advocates of a major boost in such spending — mirroring the history of past buildups — have called for simultaneously cutting taxes. With the renewal of the 2017 tax cuts all but certain, we appear to be on track for such a tax cut.

Instead of increasing taxes, many advocates of boosting defense spending have glibly and misleadingly suggested that offsetting savings can easily be found among nondefense programs. In reality, most such programs are either too small to realistically generate large savings; would involve cuts to other important national security related programs; or are highly resistant to cuts because they are too critical to too many Americans and, in key areas, linked to long-projected changes in the country’s demographics — in particular, the growth of the elderly share of the population.

Without offsetting reductions, the combination of increasing defense spending to 5 percent of GDP and implementing a major tax cut could more than triple the projected growth in the debt burden over the next three decades. Under current law and policies, federal debt held by the public is projected to grow from about 99 percent of GDP today to 166 percent of GDP by 2054. If the proposed increase in defense spending were implemented and sustained, the debt would instead grow to some 260 percent of GDP. Worse yet, implementing both the proposed increase in defense spending and tax cuts could cause the debt to jump to some 310 percent of GDP by 2054. The growth of the federal debt along these lines would substantially increase risks to the country’s long-term economic growth.

There is another path open to the new administration and Congress — one that would involve addressing the country’s existing debt burden, rather than dramatically exacerbating it. At present, the fiscal gap that would need to be closed through a combination of tax increases and entitlement reform in order to stabilize the federal debt and put the country on a sustainable path is equivalent to only about 1.5 percent of GDP. A deal of this magnitude is eminently doable — in mathematical and budgetary terms. Such an agreement would do far more to secure America’s future than would a massive military expansion built on a fragile economic foundation, hollowed out by mountains of debt. Unfortunately, instead the country appears on the verge of pursuing a set of policies that will turn a difficult but manageable problem into a far more intractable one.

Related

Program

Authors

Steven Kosiak is a non-resident fellow at the Quincy Institute and a partner at ISM Strategies in Washington, D.C. He is also a senior adjunct faculty member at American University’s School of International Service (SIS) and an adjunct senior fellow…

Citations

Valerie Insinna, “5% GDP: Top SASC Republican Pitches Dramatic Jump in Defense Spending, $55 Billion More in 2025,” Breaking Defense, May 29, 2024, https://breakingdefense.com/2024/05/5-gdp-top-sasc-republican-pitches-dramatic-jump-in-defense-spending-55b-more-in-fy25/. ↩

To account for the effects of inflation, unless otherwise noted, all spending and funding levels included in this report are expressed in 2024 dollars and all changes in those levels are expressed in real (inflation-adjusted) terms. ↩

Robert Wilkie, “There Can Be No America First Without the Shield of the Armed Forces,” in An America First Approach to U.S. National Security, ed. Fred Fleitz, (Washington: America First Press, 2024). ↩

“Commission on the National Defense Strategy,” RAND Corporation, July 29, 2024: 9 and 11, https://www.rand.org/content/dam/rand/pubs/misc/MSA3057-4/RAND_MSA3057-4.pdf. ↩

See, for example, Rachel Esplin Odell et al., “Active Denial: A Roadmap to a More Effective, Stable, and Sustainable U.S. Defense Strategy in Asia,” Quincy Institute for Responsible Statecraft, June 2022, https://quincyinst-2.s3.amazonaws.com/wp-content/uploads/2022/06/17214308/QUINCY-REPORT-ACTIVE-DENIAL-JUNE-2022-2.pdf. ↩

For a variety of reasons, including lack of transparency by the Chinese government, it is not possible to provide a precise comparison of U.S. and Chinese defense spending today. However, the best available estimates suggest that the United States currently spends roughly three times as much on its military than does China. It is also difficult to precisely compare U.S. and Soviet military spending during the Cold War, in part because of the lack of transparency in the Soviet defense budget. However, official U.S. estimates made at the time placed Soviet military spending roughly on par with, or slightly above, U.S. defense spending during the last decade of the Cold War. For an excellent discussion of Chinese military spending, see M. Taylor Fravel et al., “Estimating Chinese Defense Spending: How to Get It Wrong (and Right),” Texas National Security Review 7, no. 3 (Summer 2024): 41–54, https://tnsr.org/2024/06/estimating-chinas-defense-spending-how-to-get-it-wrong-and-right/. For data concerning U.S. and Soviet defense spending, see U.S. Department of State, Arms Control and Disarmament Agency, “World Military Expenditures and Arms Transfers, 1990,” November 1991: 81 and 85, https://2009-2017.state.gov/documents/organization/185650.pdf. ↩

Unless otherwise noted, this paper uses the Congressional Budget Office, CBO, concept of “federal debt held by the public” in all mentions of U.S. government debt or debt-to-GDP ratios. This concept refers to debt owed by the U.S. federal government that is held by the public (U.S. public or in other nations). ↩

Author’s estimate derived from a comparison of CBO’s “extended baseline scenario” — adjusted to reflect the higher discretionary spending levels included in the final 2024 budget deal reached after CBO had released its analysis — and CBO’s “constant debt-to-GDP ratio” scenario. Congressional Budget Office, “The Long-Term Budget Outlook Under Alternative Scenarios for the Economy and Budget,” May 2024: Supplementary Data, Tables 1 and 9, https://www.cbo.gov/publication/60319#_idTextAnchor000. For a discussion of the fiscal gap, see Congressional Budget Office, “Calculating the Fiscal Gap,” June 26, 2009, https://www.cbo.gov/publication/24929. ↩

Author’s estimate based on CBO and other data. ↩

“Commission on the National Defense Strategy,” RAND Corporation: 9 and 11. ↩

Congressional Budget Office, “The Long-Term Budget Outlook: 2024 to 2054,” March 2024: 12, https://www.cbo.gov/system/files/2024-03/59711-Long-Term-Outlook-2024.pdf. ↩

To be sure, some advocates of increasing defense spending to 5 percent of GDP have left open the possibility that such an increase might eventually be reversed to some degree, which would lessen the impact on the debt. And in his own proposal, Sen. Wicker has explicitly called for the increase to be temporary. In practice, however, buildups in military forces, weapons procurement, and defense research and development tend to create enormous pressure to sustain spending levels, if not further increase those levels beyond initially projected levels. Moreover, the notion that such an increase would be temporary seems to very optimistically assume that Chinese defense spending — which at present is far below U.S. defense spending as a share of GDP — would not be increased in response to such a large U.S. buildup. In any event, absent a specific plan as to when such an increase would be reversed and to what new level defense spending would then be lowered to as a share of GDP, it is difficult to take seriously assertions that it would be temporary. ↩

Author’s estimate based on CBO and other data. ↩

Author’s estimate based on CBO and other data. ↩

Consistent with this approach, the most recent House Republican budget resolution, for instance, calls for $9.3 trillion in program cuts over 10 years, almost half of which were unspecified. ↩

Congressional Budget Office, “An Update to the Budget and Economic Outlook: 2024 to 2034,” June 2024: 20, https://www.cbo.gov/publication/60039. ↩

Author’s estimate based on CBO and other data. CBO’s most recent extended baseline estimate was released in February 2024, before enactment of the final 2024 budget deal. That deal included about $80 billion in additional discretionary funding, equivalent to about 0.25 percent of GDP. Adding that spending to CBO’s original extended baseline estimate of primary spending increases that spending from an average of about 20.4 percent of GDP through 2054 to about 20.7 percent. Congressional Budget Office, “Long-Term Budget Outlook Under Alternative Scenarios,” May 2024: Supplementary Data, Table 1, https://www.cbo.gov/publication/60169#data. ↩

Author’s estimate. ↩

This may modestly understate federal primary outlays over the 2024–34 period. CBO’s long-term (2024–34) budget projections were first published in March 2024, before the enactment of the FY 2024 omnibus spending bill that funds the discretionary portion of the federal budget and is based on estimated, rather than actual, discretionary appropriations levels for FY 2024. CBO’s “Update to the Budget 2024 to 2034,” published in June 2024, incorporates the enacted discretionary appropriations levels, which are higher than the earlier, estimated levels. This data suggests that primary federal spending may grow by perhaps an additional 0.5 percent of GDP through 2034. Even with this additional growth, however, federal primary spending over the next 30 years would be projected to exceed its 2023 share of GDP by an average of only 1.2 percentage points. ↩

The projections of primary spending included in this chart — but not the projected interest costs — have been adjusted by the author to reflect the impact on CBO’s extended baseline of the higher discretionary spending levels included in the final 2024 budget deal. Thus, they somewhat understate projected spending on net interest relative to primary spending. ↩

This estimate reflects the number of elderly or disabled Americans who receive Medicare and/or Medicaid benefits. By comparison, about 56 million elderly and 7 million disabled Americans receive Social Security benefits. Since these are largely overlapping — but not identical — populations, the estimate of 75 million people may slightly understate the number of elderly or disabled Americans who receive Social Security and/or Medicare and/or Medicaid benefits. ↩

Medicare is by far the largest of the major health care programs, accounting for about 55 percent of the funding, and covers 57 million elderly and 8 million disabled individuals (virtually all of whom are also eligible for Social Security benefits). Medicaid accounts for another 37 percent of the funding, most of which is also allocated to elderly or disabled individuals (primarily low-income people who need assistance beyond what is provided by Medicare). Taken together, about three-quarters of the funding for major health care programs is allocated to the elderly or disabled. The remaining quarter of this funding is used to provide health insurance to children of low-income families through Medicaid and the Children’s Health Insurance Program, and to low-income adults through both Medicaid and Affordable Care Act premium support. ↩

The ratio is roughly 7 to 1 among Social Security beneficiaries and 8 to 1 among beneficiaries of Medicare and Medicaid (the two major health care programs that include funding for the elderly or disabled). ↩

In addition to about 56 million elderly and 7 million disabled Americans, Social Security provides benefits to about 4 million nonelderly survivors and children. Emma K. Tatem, “Social Security Overview,” Congressional Research Service, May 10, 2024: 2, https://crsreports.congress.gov/product/pdf/IF/IF10426. ↩

According to one survey, for example, 79 percent of Americans oppose cuts to Social Security and 67 percent oppose increases to the Medicare premium. Amanda Seitz et al., “Most Oppose Social Security, Medicare Cuts: AP-NORC Poll,” Associated Press, April 7, 2023, https://apnews.com/article/social-security-medicare-cuts-ap-poll-biden-9e7395e8efeab68063d741beac6ef24b. ↩

Paul N. Van de Water et. al., “Social Security Benefits Are Modest,” Center on Budget and Policy Priorities, December 7, 2023: 3, https://www.cbpp.org/sites/default/files/atoms/files/1-11-11socsec.pdf. ↩

“Policy Basics: Top Ten Facts about Social Security,” Center on Budget and Policy Priorities, May 31, 2024, https://www.cbpp.org/research/social-security/top-ten-facts-about-social-security. ↩

“Dependence on Social Security Is Striking,” Center for Retirement Research, Boston College, April 3, 2018, https://crr.bc.edu/dependence-on-social-security-is-striking/. ↩

For 2024, Medicare costs per beneficiary averaged about $14,000. This figure does not include out-of-pocket expenses for Medicare premiums, supplemental insurance, and services not covered by Medicare, which are estimated to average some $5,000 annually. ↩

Barbara A. Butrica et al., “The Disappearing Defined Benefit Pension and Its Potential Impact on the Retirement Incomes of Baby Boomers,” Social Security Bulletin 69, no. 3 (October 2009), https://www.ssa.gov/policy/docs/ssb/v69n3/index.html. ↩